Putting Portfolios Together when the World is Falling Apart

Key Takeaways

- Over the past fifty years, global equity markets have become increasingly correlated, reflecting greater international integration in goods, labor, and capital markets.

- But globalization may now be reversing. If the world deglobalizes, we would expect markets to decorrelate.

- The risk-minimizing response to deglobalization is to make portfolios as global as possible; the benefits of cross country diversification rise as cross-country correlations fall. When markets decorrelate, the imperative to diversify grows stronger.

Table of contents

For many decades, the world economy became increasingly integrated across product, labor, and capital markets—in a word, globalization. One of the many consequences of globalization was higher cross-market correlations. For example, the correlation between U.S. and German equities rose from 0.35 in the period 1970-1997 to 0.81 in the period 1998-2026.

In recent years, globalization has stalled and we now face the prospect of deglobalization. Nations are erecting barriers to the free movement of goods, labor, and capital across borders. If globalization goes into reverse, we would expect equity markets to decorrelate.

Perhaps counterintuitively, as the world deglobalizes, risk-minimizing investors should respond by making their portfolios as global as possible. A world of less-correlated equity markets is a world in which the benefits of global diversification are higher.

Globalization Raised Correlations

Globalization was a decades-long process involving falling trade barriers, increased migration, reduction in capital controls, financial liberalization, and regulatory harmonization. Milestones included the fall of the Berlin Wall (1989), NAFTA (1994), China’s entry into the WTO (2001), and the expansion of the EU (2000s).

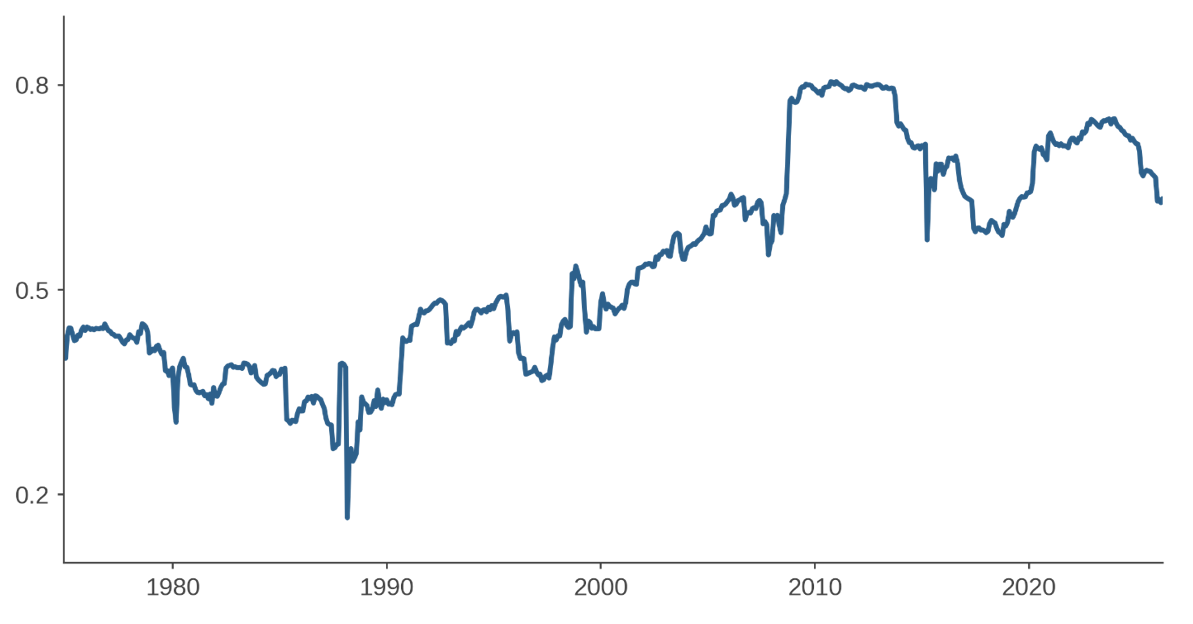

Figure 1 shows the resulting change in cross-country equity correlations from 1970 to 2026. It shows average pairwise correlations of the 23 developed market (DM) countries currently in the MSCI World Index, calculated from trailing 60-month windows of gross USD returns.1 After globalization accelerated during the 1990s, average correlations rose substantially.

The pattern is representative of the broader sweep of history. Looking at global stock returns from 1850 to 2000, Goetzmann, Li, and Rouwenhorst (2005) find that “correlations vary considerably over time and are highest during periods of economic and financial integration such as the late 19th and 20th centuries.”

Globalization seems to have stalled sometime after the Global Financial Crisis (GFC). Significant retrenchments included the Brexit vote (June 2016), Russia’s full-scale invasion of Ukraine (February 2022), and tariffs announced by the Trump administration (April 2025). It remains unclear whether globalization has actually reversed in recent years (“deglobalization”) or whether it has merely slowed (“slowbalization”).2

Figure 1: Average DM cross-country correlation

Higher Correlations, Lower Diversification Benefit

Suppose that, going forward, we see unambiguous deglobalization and the world economy returns to the lower levels of integration observed from 1970 to 1997. What would this world look like?

First, we would expect lower corporate profit growth as the global economy is impacted. Second, we would expect lower cross-country correlations. While there is little that shareholders can do to insulate themselves from weaker fundamentals, they can benefit from decorrelating markets by diversifying as much as possible.

We define the diversification benefit as the reduction in portfolio volatility achieved by holding a diversified portfolio instead of a single country. Under simplifying assumptions, this benefit is a straightforward function of correlation.3

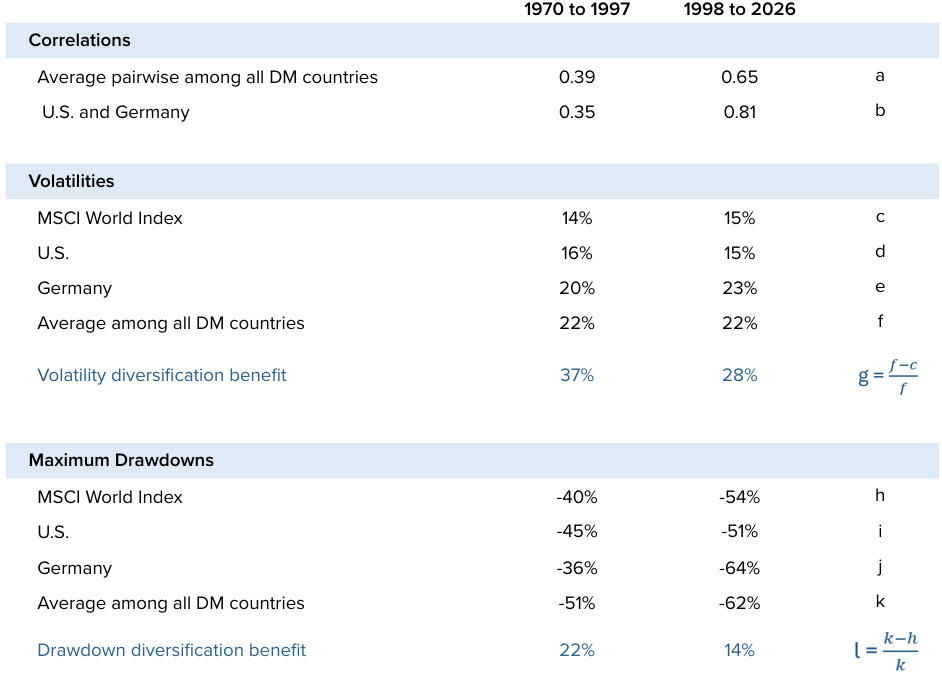

Table 1: Benefits of Diversification – Developed Market Equities

Average developed market correlation rose from 0.39 before 1998 to 0.65 after 1998 (Table 1, row a). This increase implies that the diversification benefit was about 1.9 times greater before 1998 than after 1998.4

Table 1 fleshes out this change. Before 1998, the MSCI World portfolio had a return volatility of 14% (row c), 37% lower than the 22% average volatility of its constituent countries (rows f and g). After 1998, the benefit of diversification declined to 28%. While not the full 1.9x implied by the correlations, the earlier period still shows a meaningfully larger benefit (1.3x). 5

Another way to measure diversification is through its impact on drawdowns, which we would expect to be roughly proportional to volatility. Table 1 shows that diversification reduced maximum drawdowns by 22% before 1998 and 14% after (row l). Again, the benefits of diversification were substantially larger in the earlier period (1.6x greater).

Table 1 also highlights results for the U.S. and Germany. Investors sometimes argue that global diversification is useless, and that it is sufficient to hold only U.S. equities. At first glance, the post-1998 data in Table 1 appears to support this claim, since during that period the U.S. had a smaller maximum drawdown (51%, row i) than the world portfolio (54%, row h) and similar volatility.

However, it would be a mistake to hold a portfolio that is 100% U.S. equities. It is not a law of nature that the U.S. always has lower risk than the world index. Before 1997, Table 1 shows the U.S. had drawdowns and volatility that were higher than the world index. Trailing performance can be a misleading guide to the future. For example, before 1998, the country with the mildest drawdown was Germany (-36%, row j). But after 1998, Germany had a drawdown that was worse than average DM country and worse than the world index.

Conclusion

Deglobalization, if it occurs, will produce winners and losers. Which countries will be the winners? We don’t know. The appropriate response, therefore, is to diversify across countries.6

Will deglobalization lead to a collapse of dollar dominance and wild fluctuations in exchange rates? Again, we don’t know. By holding a world portfolio, we diversify across currencies, helping to protect wealth from monetary disruption.

It has been said that diversification is the only free lunch in finance. While the free lunch of global diversification is always valuable, it becomes especially nutritious when markets fragment and correlations decline. If you want to minimize risk, then you should diversify more—not less—when markets decorrelate.

References

Altman, Steven A., and Caroline R. Bastian. “DHL Global Connectedness Report 2026.” DHL Global Connectedness Report (2026).

Bergstrom, Gary. “A new route to higher returns and lower risks.” Journal of Portfolio Management, Fall 1975.

Campbell, John Y. Financial decisions and markets: A course in asset pricing. Princeton University Press, 2017.

Elton, Edwin J., and Martin J. Gruber. “Risk reduction and portfolio size: An analytical solution.” The Journal of Business 50, no. 4 (1977): 415-437.

Fernández-Villaverde, Jesús, Tomohide Mineyama, and Dongho Song. Are we fragmented yet? Measuring geopolitical fragmentation and its causal effect. NBER Working Paper No. 32638. National Bureau of Economic Research, 2024.

Goetzmann, William N., Lingfeng Li, and K. Geert Rouwenhorst. “Long-term global market correlations.” The Journal of Business 78 (2005): 1-38.

Michaud, Richard O., Gary L. Bergstrom, Ronald Frashure, and Brian Wolahan. “Twenty years of international equity investing.” Journal of Portfolio Management 23, no. 1 (1996).

Mohr, Cathrin, and Christoph Trebesch. “Geoeconomics.” Annual Review of Economics 17 (2025).

Endnotes

- Similar results are shown in “Polarizing Views: China’s Impact on EM Investing,” Acadian, December 2021.

- See Mohr and Trebesch (2025) for a literature review. Fernández-Villaverde, Mineyama, and Song (2024) argue that deglobalization has already begun while Altman and Bastian (2026) say that “deglobalization is a clear risk, but at least for now, the world’s connectedness is holding steady at a historically high level.”

- Following Elton and Gruber (1977), for a portfolio with

equally weighted assets where each asset has a return variance

equally weighted assets where each asset has a return variance  and an identical pairwise return correlation of

and an identical pairwise return correlation of  , the portfolio variance reduces to:

, the portfolio variance reduces to:  This equation can also be found in many finance textbooks, for example as equation 2.56 in Campbell (2017).

This equation can also be found in many finance textbooks, for example as equation 2.56 in Campbell (2017). - For large

, the standard deviation is lower by a factor of approximately

, the standard deviation is lower by a factor of approximately  relative to a single asset portfolio. The diversification benefit is higher by

relative to a single asset portfolio. The diversification benefit is higher by  =1.94.

=1.94. - The substantial benefit of international diversification prior to 1998 was highlighted by Bergstrom (1975) and Michaud, Bergstrom, Frashure, and Wolahan (1996). In fact, the observation helped to motivate Bergstrom’s founding of Acadian Asset Management in 1986.

- In addition to deglobalization, another source of uncertainty is AI. Which countries will be AI winners? Since we don’t know the answer, the risk-minimizing choice is to hold all countries.

Legal Disclaimer

These materials provided herein may contain material, non-public information within the meaning of the United States Federal Securities Laws with respect to Acadian Asset Management LLC, Acadian Asset Management Inc. and/or their respective subsidiaries and affiliated entities. The recipient of these materials agrees that it will not use any confidential information that may be contained herein to execute or recommend transactions in securities. The recipient further acknowledges that it is aware that United States Federal and State securities laws prohibit any person or entity who has material, non-public information about a publicly-traded company from purchasing or selling securities of such company, or from communicating such information to any other person or entity under circumstances in which it is reasonably foreseeable that such person or entity is likely to sell or purchase such securities.

Acadian provides this material as a general overview of the firm, our processes and our investment capabilities. It has been provided for informational purposes only. It does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or to purchase, shares, units or other interests in investments that may be referred to herein and must not be construed as investment or financial product advice. Acadian has not considered any reader's financial situation, objective or needs in providing the relevant information.

The value of investments may fall as well as rise and you may not get back your original investment. Past performance is not necessarily a guide to future performance or returns. Acadian has taken all reasonable care to ensure that the information contained in this material is accurate at the time of its distribution, no representation or warranty, express or implied, is made as to the accuracy, reliability or completeness of such information.

This material contains privileged and confidential information and is intended only for the recipient/s. Any distribution, reproduction or other use of this presentation by recipients is strictly prohibited. If you are not the intended recipient and this presentation has been sent or passed on to you in error, please contact us immediately. Confidentiality and privilege are not lost by this presentation having been sent or passed on to you in error.

Acadian’s quantitative investment process is supported by extensive proprietary computer code. Acadian’s researchers, software developers, and IT teams follow a structured design, development, testing, change control, and review processes during the development of its systems and the implementation within our investment process. These controls and their effectiveness are subject to regular internal reviews, at least annual independent review by our SOC1 auditor. However, despite these extensive controls it is possible that errors may occur in coding and within the investment process, as is the case with any complex software or data-driven model, and no guarantee or warranty can be provided that any quantitative investment model is completely free of errors. Any such errors could have a negative impact on investment results. We have in place control systems and processes which are intended to identify in a timely manner any such errors which would have a material impact on the investment process.

Acadian Asset Management LLC has wholly owned affiliates located in London, Singapore, and Sydney. Pursuant to the terms of service level agreements with each affiliate, employees of Acadian Asset Management LLC may provide certain services on behalf of each affiliate and employees of each affiliate may provide certain administrative services, including marketing and client service, on behalf of Acadian Asset Management LLC.

Acadian Asset Management LLC is registered as an investment adviser with the U.S. Securities and Exchange Commission. Registration of an investment adviser does not imply any level of skill or training.

Acadian Asset Management (Singapore) Pte Ltd, (Registration Number: 199902125D) is licensed by the Monetary Authority of Singapore. It is also registered as an investment adviser with the U.S. Securities and Exchange Commission.

Acadian Asset Management (Australia) Limited (ABN 41 114 200 127) is the holder of Australian financial services license number 291872 ("AFSL"). It is also registered as an investment adviser with the U.S. Securities and Exchange Commission. Under the terms of its AFSL, Acadian Asset Management (Australia) Limited is limited to providing the financial services under its license to wholesale clients only. This marketing material is not to be provided to retail clients.

Acadian Asset Management (UK) Limited is authorized and regulated by the Financial Conduct Authority ('the FCA') and is a limited liability company incorporated in England and Wales with company number 05644066. Acadian Asset Management (UK) Limited will only make this material available to Professional Clients and Eligible Counterparties as defined by the FCA under the Markets in Financial Instruments Directive, or to Qualified Investors in Switzerland as defined in the Collective Investment Schemes Act, as applicable.