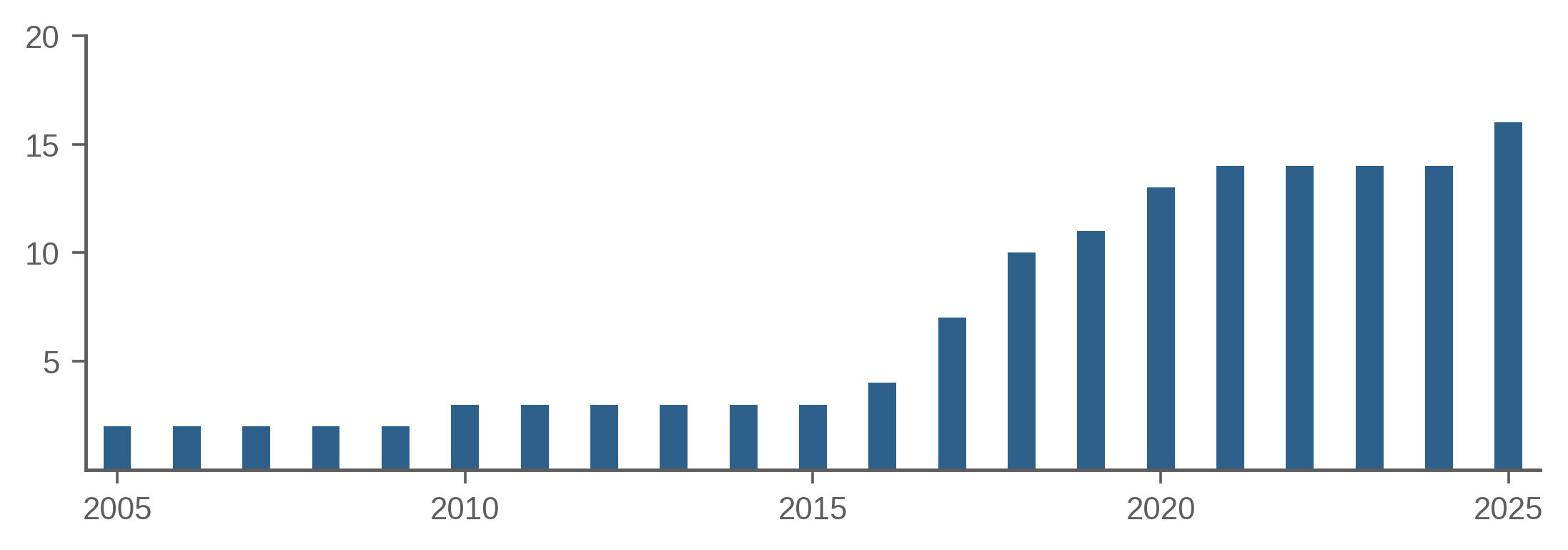

Systematic credit investing has grown meaningfully over the past decade. The number of dedicated systematic strategies has increased (Figure 1), allocators are increasingly allocating to them, and traditional discretionary managers are integrating systematic elements into their investment processes. This growth has been supported by electronification of corporate bond markets and advances in AI, which are improving implementation efficiency, expanding the investable universe, and accelerating quantitative credit research.

To understand why these trends are supportive of systematic credit, we must first clarify what we mean by the term. In the broader world of corporate bonds, “systematic credit” has become an ambiguous catch-all label for almost any application of quantitative methods to trading, investing, or risk management, including hedge funds, systematic asset managers, smart beta strategies, quantamental approaches, and even market making. In this note, we use systematic credit more precisely to describe fundamentally driven, benchmark-relative corporate bond strategies that apply purely quantitative methods and a rules-based approach to bond selection and portfolio construction.

In the discussion that follows, we describe why electronification and AI are especially favorable to systematic investing in credit markets and how managers’ success will depend on their ability to integrate new technologies and adapt to a changing market structure.

Figure 1: Number of Asset Managers with Dedicated Systematic Credit Offerings

Source: Acadian based on data from eVestment. Active systematic asset managers were selected based on products in eVestment with a credit focus and “systematic” or “factor” in the product name. A limited number of additional managers were included based on knowledge of systematic credit offerings at large quantitative firms. Firms are included in the sample for a given year only if they maintained active strategies throughout the entire year. For illustrative purposes only. Please see additional disclosure at the end of this document.

Source: Acadian based on data from eVestment. Active systematic asset managers were selected based on products in eVestment with a credit focus and “systematic” or “factor” in the product name. A limited number of additional managers were included based on knowledge of systematic credit offerings at large quantitative firms. Firms are included in the sample for a given year only if they maintained active strategies throughout the entire year. For illustrative purposes only. Please see additional disclosure at the end of this document.

Electronification of Corporate Credit Markets

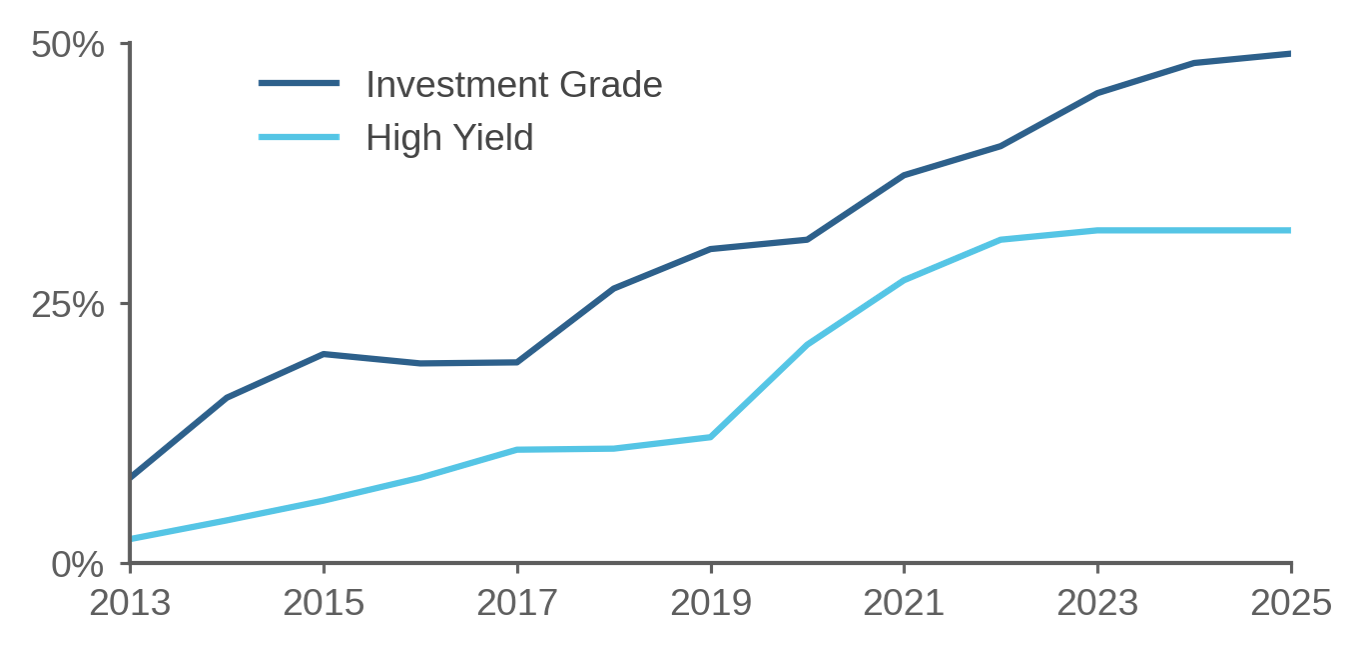

Electronic execution has steadily gained share in corporate bond trading, which even a decade ago was still dominated by manual, voice-based workflows (Figure 2). This shift has materially changed the structure of public credit markets, increasing trading volumes and broadening participation. Dealers now use algorithmic pricing to respond to quote requests and facilitate portfolio trades. These more efficient and scalable execution mechanics have increased liquidity, reduced trading frictions, and improved price discovery.

Figure 2: Share of Electronic Corporate Bond Trading in the U.S.

Source: Acadian based on data from Coalition Greenwich MarketView. For illustrative purposes only.

Beyond its effects on trading, electronification has also improved the quantity and quality of available credit market data, an equally important if less visible development. This has enabled more precise modeling of liquidity, fill probabilities, and market impact, as well as more rigorous ex post evaluation of execution quality.

The associated reductions in execution costs and risks have benefited all market participants, but they are especially important for systematic managers. Systematic credit strategies tend to have higher turnover than discretionary approaches, which magnifies the impact of lower execution costs.

A second advantage for systematic managers stems from the importance of “breadth” to their investment approach, whether in the context of credit or equity markets. Greater liquidity and transparency have expanded the investable universe, increasing the number of independent investment views that managers can express and enhancing their flexibility to translate those insights into active portfolio positions.1 Systematic managers are especially well positioned to benefit from these developments because their forecasting and portfolio construction approaches are built to scale. In contrast, discretionary managers typically face higher incremental research and implementation costs when expanding coverage.

Despite the improvements associated with electronification, corporate bond markets remain murky and complex. As in the equity world, liquidity is dispersed across venues. But unlike in equities, there is no guarantee of best execution or even a consolidated market view. Adding to this opacity, anonymous trading protocols can obscure counterparty visibility and increase adverse selection risk.

As a result, systematic credit managers face important decisions about their investment in implementation. The extent to which they benefit from electronification will depend on how effectively they aggregate fragmented liquidity information, model market impact and liquidity risk, and develop the technologies, methodologies, and relationships needed to access execution opportunities efficiently.

AI in Active Credit Investing

AI has long been part of the systematic investor’s analytical toolkit, though the underlying methods were not always labeled as AI. For more than a decade, systematic managers have used techniques such as machine learning and natural language processing to enhance return forecasts and model risk.

Systematic credit is no exception. In forecasting individual bond returns, AI is used to increase the flexibility and precision of predictive models. It is integral to the extraction of signals from diverse forms of structured and unstructured alternative data, including regulatory filings, earnings-call transcripts, and news reports. AI is also used to model subtle but economically important relationships across issuers.

The advances in generative AI, however, have rapidly changed how research is done in systematic credit. Until recently, managers largely had to build their own AI capabilities from publicly available libraries. Today, they can purchase access to sophisticated AI platforms that are more capable than systems that even large managers could have developed internally just a few years ago. Once a do-it-yourself activity, working with AI now involves engaging with a rapidly evolving industrial ecosystem of models, data providers, and software platforms.

Perhaps even more consequential, modern AI tools are dramatically streamlining data processing, code generation, and iterative testing, accelerating cycles of hypothesis generation and evaluation. Conversational AI assistants significantly eased programming in recent years, and newer agentic systems now allow researchers to create analytical machinery using natural language. As a result, the level of programming expertise required to execute sophisticated quantitative research has fallen.

But as with electronification, the advances in AI hardly guarantee success in credit investing. Crucially, AI does not replace judgment in knowing what analytical tools to build or how to evaluate whether they have been implemented correctly. Even if researchers no longer write each line of code themselves, they must be able to verify and adapt AI-generated code. AI agents can produce outputs that appear correct while violating intended analytical safeguards.

Researchers also still need expertise and judgment in developing meaningful hypotheses, understanding their data, choosing appropriate statistical tests, avoiding lookahead and other biases in analysis, and interpreting results. As technical barriers to conducting analysis fall, the risks of misguided, redundant, and faulty research rise.

In addition, larger firms with established systematic research platforms have advantages of scale in the application of AI and alternative data. One is cost. While the price of access to AI models has fallen, the cost of data continues to rise. Firms that cannot afford to spend millions of dollars on input information may not be able to compete. But data access alone is not enough. Managers also need industrialized research infrastructure to manage data resources over time and to conduct analysis with consistent rigor. Moreover, AI is likely to magnify the benefits of firms’ proprietary data and insights.

In summary, while access to sophisticated AI tools is becoming increasingly democratized, the benefits will not accrue uniformly across managers. Success will depend on access to differentiated data, the quality and robustness of research infrastructure, and the organizational capabilities needed to evaluate and deploy new technologies efficiently. Firms that have already invested heavily in these resources are likely to enjoy a meaningful advantage. At the same time, democratization of access to powerful AI tools does not diminish the importance of investment acumen, research expertise, and disciplined process. While AI lowers certain technical barriers to quantitative research, it does not replace the skills required to formulate hypotheses, evaluate evidence, and allocate research resources effectively.

Conclusion: Structural Change and the Future of Systematic Credit

Corporate bond markets are evolving in ways that increasingly favor systematic approaches. Electronification has improved liquidity, lowered trading frictions, and expanded the investable universe. Advances in AI and data-intensive research methods are improving the speed, scale, and sophistication of return forecasting. Together, these developments strengthen the core drivers of active performance: forecast accuracy, breadth, and implementation efficiency.

But these same developments are also reshaping competition within systematic credit because their benefits are unlikely to accrue uniformly across managers. Firms with differentiated data, robust research infrastructure, deep investment and research expertise, and sophisticated implementation capabilities will be best positioned to benefit from these changes.

Don't miss the next Acadian Insight

Get our latest thought leadership delivered to your inbox