America’s geriatric stock market

America is aging. The median age of U.S. residents increased from 30 years in 1980 to 39 years in 2024. Oddly enough, this trend in America’s human population is mirrored in America’s equity population. By some measures, the age of the U.S. stock market is near all-time highs. For both the human and the equity populations, the main cause of this aging is lack of new entrants (babies for humans, new issues for equities).

Should we be alarmed by our elderly stock market? Does it reflect declining American dynamism, an ossifying corporate hierarchy, and rising market decrepitude? Should you dump U.S. stocks and shop around for a younger market? No. Rising age may be undesirable for human populations, but for equity markets, lack of young firms indicates high future returns. Based only on its age, today’s geriatric market is a screaming buy.

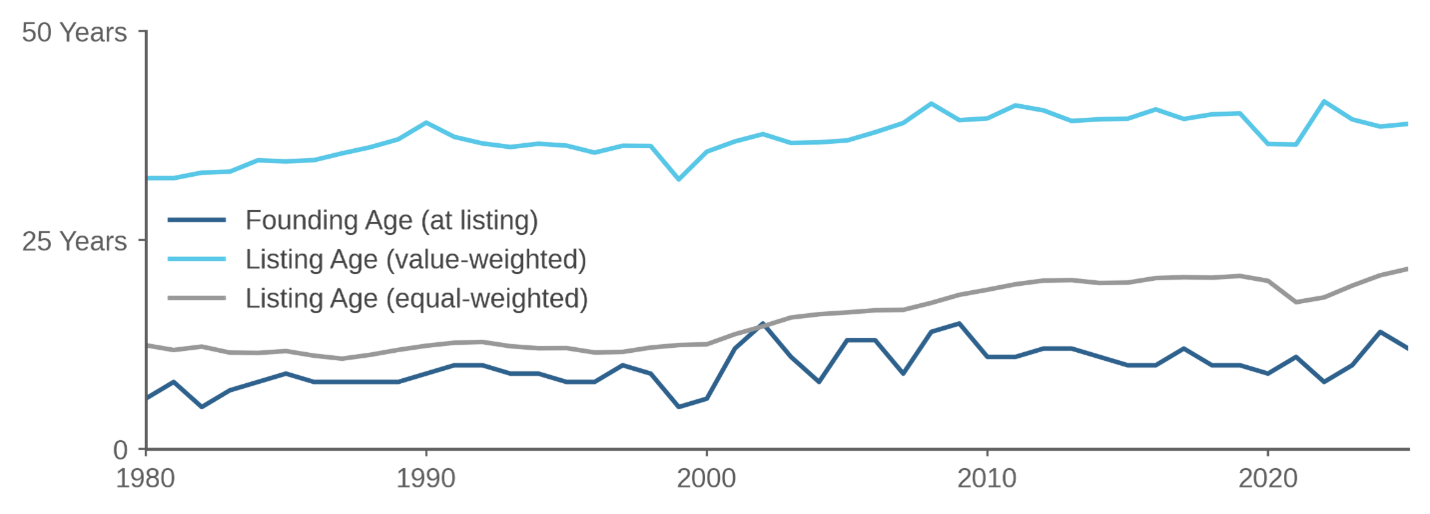

Consider Microsoft.[1] Microsoft was founded on April 4, 1975, and thus its current founding age is 50.9 years. Its IPO was March 13, 1986, and thus its current listing age is 40. It turns out that Microsoft is representative of the cap-weighted U.S. stock market both in its current listing age and its founding age at IPO.

Figure 1 shows the average listing age of U.S. common stocks from 1980 to 2025, using either value-weighted or equally-weighted averages. It also shows median founding age for operating firm IPOs, from Professor Jay Ritter’s data.

The rising trend in all three age measures is clear. As I’ve previously discussed, the number of IPOs has declined since 2000, resulting in a decrease in the total number of listed firms and an increase in listing age.[2] Founding age at listing has also risen (an extreme example being the recent IPO of Birkenstock, founded in 1774). One explanation is that the growth of private markets has caused firms to stay private longer, as discussed in Huang, Ritter, and Zhang (2023).

Figure 1: Age of U.S. common stock

All three age measures tend to fall during new issue waves, with value-weighted listing age falling partly due to new issues and partly due to younger firms rising in price relative to older firms. Greenwood, Shleifer, and You (2019) find that when young firms outperform, that’s a symptom of an emerging bubble.

Exuberant stock markets involve exciting new technology, new personalities, new investors, and new firms. Markets with many young firms tend to be overvalued, because private firms rush to go public to take advantage of high equity prices.

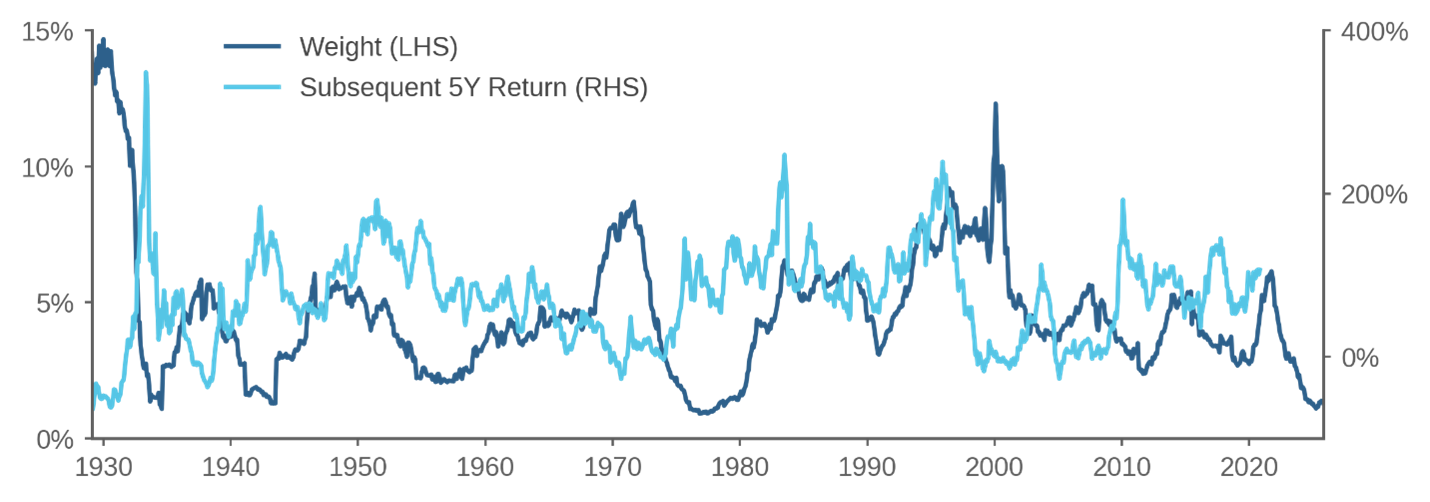

Figure 2: New issue weight vs. subsequent market return

Another way to measure market composition is the new issue weight, defined as the percent of the stock market’s total capitalization that has listing age less than three years. Figure 2 shows the new issue weight from 1929 to 2025 and is an update of a similar figure in Lamont (2002).[3] When the new issue weight goes up, that means the market is getting younger as new entrants arrive or as recent entrants outperform the market.

Let me give you a whirlwind tour of the history of new issue waves as seen in Figure 2:

- A huge new issue wave in 1929 with weight peaking over 14% in January 1930.

- A smaller new issue wave in 1968/1969, which Graham (1973) condemned as an “unprecedented outpouring of issues of lowest quality” and which was depicted in season six of Mad Men when the fictional firm of Sterling Cooper Draper Pryce planned an IPO. Weight subsequently peaked over 8% in September 1971.

- A giant wave during the tech stock bubble, with weight peaking over 12% in February 2000.

- A relatively modest wave with weight peaking over 6% in October 2021.

As of November 2025, the new issue weight is 1.3%, far below the historical average of 4.6%. Relatively few firms have gone public in the past three years, and those firms currently have low valuations. While today’s low weight partly reflects the long-term decline in the propensity to go public, it’s still striking that the weight has fallen so dramatically just in the past three years. It’s not just that we don’t have a new issue wave; what we have is an epic new issue drought.

Prior to the current drought, the only years in U.S. history with lower new issue weight were 1934, 1976, 1977, and 1978; times when the U.S. stock market was dirt cheap. Those were fabulous buying opportunities; the dashed line in Figure 2 shows subsequent five-year cumulative market returns. The correlation of the two lines in Figure 2 is -0.37; young markets have low subsequent returns.

In Lamont (2002), I ran a regression that predicted one-month ahead market returns with the new issue weight from 1929 to 2001. I found that the weight:

… is a powerful forecaster of future returns … when the market is overweight in new lists, market excess returns are subsequently low. These results suggest that firms issue equity when expected returns on equity are low (or when equity prices are high).

In the out-of-sample period from 2001 to 2026, the new issue weight continued to work well as a market predictor, correctly identifying 2021 as a bad time to buy stocks. The regression currently predicts high returns going forward.

Of course, unlike in the late 1970s, the market currently does not look cheap based on valuation ratios, and it is entirely possible that the new issue weight is no longer a reliable predictor due to the rise of private markets. But one thing’s for sure: seen through the lens of corporate issuance, today’s stock market looks nothing at all like the 1990s. Instead, the U.S. stock market is a silver fox like George Clooney: old but attractive.

Endnotes

[1] References to this and other companies should not be interpreted as recommendations to buy or sell specific securities. Acadian and/or the author of this post may hold positions in one or more securities associated with these companies.

[2] For more details on the number and composition of listed firms, see Mauboussin and Callahan (2023) and Doidge, Karolyi, Shen, and Stulz (2025).

[3] Any firms entering in August 1962 (when CRSP added coverage for stocks from the American Stock Exchange) and January 1973 (when CRSP added NASDAQ) are classified as old, as are the Baby Bells in 1984.

References

Doidge, Craig, George Andrew Karolyi, Kris Shen, and René M. Stulz. "Are there too few publicly listed firms in the US?." Financial Review 60, no. 2 (2025): 317-329.

Greenwood, Robin, Andrei Shleifer, and Yang You. "Bubbles for Fama." Journal of Financial Economics 131.1 (2019): 20-43.

Graham, Benjamin. The Intelligent Investor. 1973.

Huang, Rongbing, Jay R. Ritter, and Donghang Zhang. "IPOs and SPACs: recent developments." Annual Review of Financial Economics 15, no. 1 (2023): 595-615.

Lamont, Owen. Evaluating value weighting: Corporate events and market timing. No. w9049, National Bureau of Economic Research, 2002.

Mauboussin, Michael J., and Dan Callahan. "Birth, Death, and Wealth Creation." Counterpoint Global Insights (2023)

Legal Disclaimer

These materials provided herein may contain material, non-public information within the meaning of the United States Federal Securities Laws with respect to Acadian Asset Management LLC, Acadian Asset Management Inc. and/or their respective subsidiaries and affiliated entities. The recipient of these materials agrees that it will not use any confidential information that may be contained herein to execute or recommend transactions in securities. The recipient further acknowledges that it is aware that United States Federal and State securities laws prohibit any person or entity who has material, non-public information about a publicly-traded company from purchasing or selling securities of such company, or from communicating such information to any other person or entity under circumstances in which it is reasonably foreseeable that such person or entity is likely to sell or purchase such securities.

Acadian provides this material as a general overview of the firm, our processes and our investment capabilities. It has been provided for informational purposes only. It does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or to purchase, shares, units or other interests in investments that may be referred to herein and must not be construed as investment or financial product advice. Acadian has not considered any reader's financial situation, objective or needs in providing the relevant information.

The value of investments may fall as well as rise and you may not get back your original investment. Past performance is not necessarily a guide to future performance or returns. Acadian has taken all reasonable care to ensure that the information contained in this material is accurate at the time of its distribution, no representation or warranty, express or implied, is made as to the accuracy, reliability or completeness of such information.

This material contains privileged and confidential information and is intended only for the recipient/s. Any distribution, reproduction or other use of this presentation by recipients is strictly prohibited. If you are not the intended recipient and this presentation has been sent or passed on to you in error, please contact us immediately. Confidentiality and privilege are not lost by this presentation having been sent or passed on to you in error.

Acadian’s quantitative investment process is supported by extensive proprietary computer code. Acadian’s researchers, software developers, and IT teams follow a structured design, development, testing, change control, and review processes during the development of its systems and the implementation within our investment process. These controls and their effectiveness are subject to regular internal reviews, at least annual independent review by our SOC1 auditor. However, despite these extensive controls it is possible that errors may occur in coding and within the investment process, as is the case with any complex software or data-driven model, and no guarantee or warranty can be provided that any quantitative investment model is completely free of errors. Any such errors could have a negative impact on investment results. We have in place control systems and processes which are intended to identify in a timely manner any such errors which would have a material impact on the investment process.

Acadian Asset Management LLC has wholly owned affiliates located in London, Singapore, and Sydney. Pursuant to the terms of service level agreements with each affiliate, employees of Acadian Asset Management LLC may provide certain services on behalf of each affiliate and employees of each affiliate may provide certain administrative services, including marketing and client service, on behalf of Acadian Asset Management LLC.

Acadian Asset Management LLC is registered as an investment adviser with the U.S. Securities and Exchange Commission. Registration of an investment adviser does not imply any level of skill or training.

Acadian Asset Management (Singapore) Pte Ltd, (Registration Number: 199902125D) is licensed by the Monetary Authority of Singapore. It is also registered as an investment adviser with the U.S. Securities and Exchange Commission.

Acadian Asset Management (Australia) Limited (ABN 41 114 200 127) is the holder of Australian financial services license number 291872 ("AFSL"). It is also registered as an investment adviser with the U.S. Securities and Exchange Commission. Under the terms of its AFSL, Acadian Asset Management (Australia) Limited is limited to providing the financial services under its license to wholesale clients only. This marketing material is not to be provided to retail clients.

Acadian Asset Management (UK) Limited is authorized and regulated by the Financial Conduct Authority ('the FCA') and is a limited liability company incorporated in England and Wales with company number 05644066. Acadian Asset Management (UK) Limited will only make this material available to Professional Clients and Eligible Counterparties as defined by the FCA under the Markets in Financial Instruments Directive, or to Qualified Investors in Switzerland as defined in the Collective Investment Schemes Act, as applicable.

About the Author