Returns to ESG Investing: Looking for the Light

Key Takeaways

- A fundamental question for investors is whether ESG investment involves a tradeoff, a combination of environmental philanthropy and reduced financial returns, or whether ESG investment will simply deliver the best returns to investors.

- An examination of “green” U.S. municipal bonds suggests a modest tradeoff. In this market investors sacrifice return, albeit to a very small extent at a rate of less than 10 basis points per annum, in exchange for holding green securities.

- In equity markets, where fundamental value is much harder to estimate, we believe that investors are only beginning to fully assess the benefits of positive environmental practices, which may generate profit, reduce risk, capture technological innovation, and avoid the costs of environmental disasters and future public policy.

8 min

Table of contents

July 2020

There is an old joke that goes roughly like this: A Good Samaritan sees a man searching for his house keys under a streetlight. She offers to help and asks whether the man is sure that he lost his keys in this particular spot. The man replies, no, that he lost them in the dark alley across the street. Why then is he looking here, under this particular streetlight, she asks. He replies: This is where the light is.

Sometimes it can be hard to find evidence to precisely answer the most fundamental questions. It’s not quite as stark as in the old joke, but there is a choice whether to make rough and direct guesses about an important debate, or instead find precise but indirect evidence. When it comes to understanding the impact of environmental, social, and governance (ESG) considerations on capital markets, it is hard to answer the fundamental questions: What impact have they had so far on market prices? And what sort of returns might these mandates deliver in the future?

Common rationales for ESG investing

There are three common rationales for ESG investing. The first is a double bottom line. Yes, investors seek to maximize their financial returns, but, for some, returns are just one part of their objective. As important is the impact of these dollars on broader societal issues such as the environment. Investors who hold such values might accept a lower return in exchange for better environmental outcomes.1

A second rationale is doing well by doing good. This rationale sees no tradeoff between financial and societal objectives. Patagonia can sell more clothes to its customers by emphasizing the ecological benefits of their manufacturing processes, for example. Or, more directly, a focus on environmental or social objectives ultimately leads to lower costs, for example as technology improves or costly litigation, oil spills, and mining disasters are avoided.

A third rationale is that change is coming. Through regulation and taxation, policy makers around the world will step in to charge producers for their negative impact on the local environment and their contribution to global climate change -- perhaps to the point that they become wholly uneconomic, stranding legacy corporate assets.2

These last two rationales require a certain degree of market inefficiency – in other words, that investors as a group are missing something now that they will see later. There is a subtle difference. For the second rationale, the evidence is already accumulating. While, for both to have full effect, the rest of the investment world must eventually wake up to the potential of ESG, its direct benefits to corporate profits, and its avoidance of a wide range of downside risks. The massive shifting of investment dollars away from polluting technologies that ensues would deliver returns for those ESG-minded investors who are in front of the wave.

A fundamental question for investors is whether ESG investment involves a tradeoff, a combination of environmental philanthropy – akin to a donation to the Sierra Club or Greenpeace – and reduced financial returns. Or whether ESG investment will simply deliver the best returns to investors, whether they are environmentally minded or not, leaving aside any ancillary, non-financial benefits.

What we know so far from municipal bonds

So, which is it?

Equity markets are like the dark alley where the man lost his keys. It is tempting to point to the recent returns of ESG funds as proof that there is no tradeoff, that a focus on ESG investing leads both to a better environment and higher returns. The Wall Street Journal reported on May 12 that “more than 70% of ESG funds across all asset classes performed better than their counterparts during the first four months of the year” as investors funneled more than $12 billion into these funds. But, this is simply a rough guess. It is conceivable that the returns, stemming from overweights to large technology firms and underweights to energy stocks, are simple good luck, with these companies positioned well to weather the global pandemic. The logic of ESG investing is about weathering regulatory and environmental change, not the spread of coronaviruses. It would be easier to declare victory if it were a resumption of U.S. commitment to the Paris Climate Agreement behind collapsing demand for oil. And yet, although the chain of causality is murky at best, the recent economic fallout does point to the vulnerability of energy companies to a demand disruption that a substantial carbon tax would bring. Moreover, it is hard to say whether ESG-oriented investments are now trading at prices that suggest lower future returns or whether we are still early in the market’s understanding of their opportunities and risks.

One place where the streetlight shines much brighter is in the municipal bond market. There, we can see a vast array of “green” and ordinary bonds issued by municipalities in pursuit of the “E” in ESG that allow for a more precise control for maturity, risk, and other attributes of these fixed income investments.3

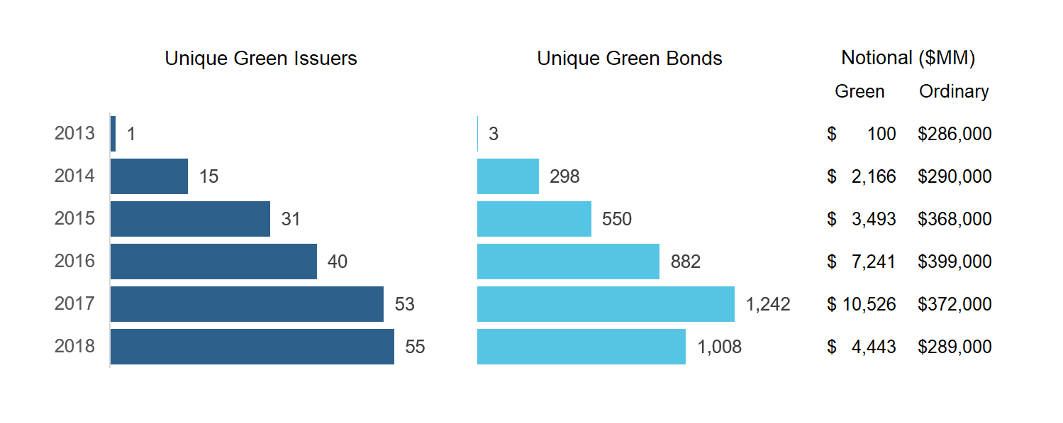

In a recent paper, we (Baker, Bergstresser, Serafeim, and Wurgler) examine data on over $27 billion in municipal bonds issued during the period from 2013 through 2018 by 195 issuers, shown in Figure 1. This remains a small drop in the bucket of more than two trillion in issuance of ordinary bonds over the same period.

Figure 1: The market for green U.S. municipal bonds

Source: Malcolm Baker, Daniel Bergstrasser, George Serafim, and Jeffrey Wurgler, “Financing the Response to Climate Change: The Pricing and Ownership of U.S. Green Bonds,” Working Paper, 2020. Data on municipal bonds come from Mergent and data on corporate bonds come from Bloomberg. Within each category of bonds, data from Bloomberg are used to identify green bonds. Floating-rate bonds are excluded. Dollar values are nominal par issuance amounts and are not adjusted for inflation. For illustrative purposes only.

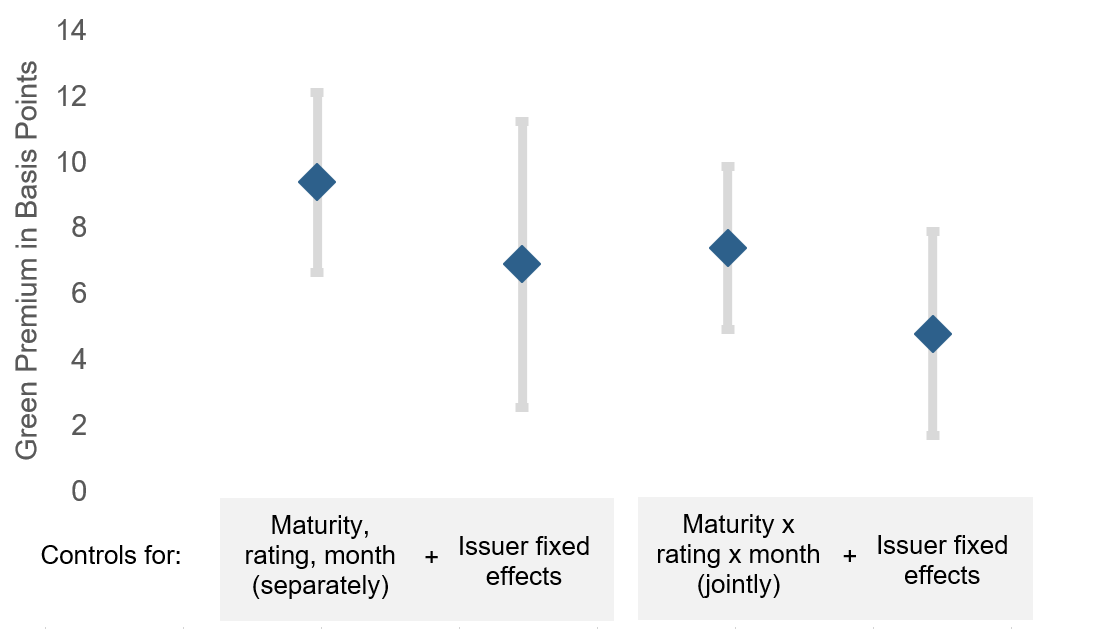

We find that these green bonds are issued at a premium in Figure 2. Although yields to maturity on green bonds are slightly higher at a median pre-tax yield of 2.48% versus 2.34% for ordinary bonds, these yields shift to a discount – and a price premium – with a large battery of controls for credit ratings, maturity, and a variety of other contractual features. But, the premium is slight, ranging from 4.8 to 9.4 basis points per annum.

Figure 2: A green price premium

Difference in yields at issue on green versus ordinary municipal bonds

Source: Malcolm Baker, Daniel Bergstrasser, George Serafim, and Jeffrey Wurgler, “Financing the Response to Climate Change: The Pricing and Ownership of U.S. Green Bonds,” Working Paper, 2020. Data on municipal bonds come from Mergent and data on corporate bonds come from Bloomberg. Within each category of bonds, data from Bloomberg are used to identify green bonds. Floating-rate bonds are excluded. Dollar values are nominal par issuance amounts and are not adjusted for inflation. For illustrative purposes only.

We also find that ownership of green bonds is more concentrated, suggesting that, so far, a smaller number of investors, perhaps those willing to make a small tradeoff between financial and environmental payoffs, specialize in holding green securities. An interesting side effect is that this yield benefit spills over to simultaneously issued ordinary bonds, suggesting that, rather than capturing the full benefit in a green price premium, municipal treasurers and their bankers spread the impact of green demand across simultaneous issuance. In so doing, they obscure the price premium (and hence lower future return) associated with green securities.4 Once green and ordinary bonds are issued at similar yields, the green bonds subsequently trade towards a premium relative to the ordinary bonds in the secondary market. Perhaps this pattern reflects a desire to give ESG bond investors the impression that there is no tradeoff between investing to maximize environmental benefits and investing to maximize returns. Our conversations with practitioners revealed this concern – that even a small headline difference in yields might scare investors from green bonds. This suggests that the willingness of investors to trade environmental considerations for return is small.

Under the streetlight of municipal bonds, our findings suggest a modest tradeoff, that investors sacrifice return, albeit to a very small extent at a rate of less than 10 basis points per annum, in exchange for holding green securities.

The broader lessons for equity markets

What about in the darker alley of equities?

There are some reasons that equity markets might be the same. Equity investors, like municipal bond investors, have a double bottom line. Money is flowing into ESG equity funds, as investors take into account not only financial but also environmental concerns, pushing the stock prices of green stocks up relative to their future fundamentals. If equity markets are otherwise informationally efficient – a very big “if” that runs counter to our investment philosophy at Acadian – the evidence from the municipal bond market would suggest that this demand is likely to have at least a small amount of upward pressure on prices and thus downward pressure on future returns.

However, there are perhaps even more reasons to suggest that equity markets are different.5 Equity investors are only slowly waking up to the idea that green firms can do well by doing good. There is no way of saying, as we can in the municipal bond market, whether investors have overreacted, pushing up prices, or underreacted, with a much greater realignment to come, because we do not know the expected future fundamentals of stocks with anywhere near the same certainty as we do for the contractual coupon payments, backed by the tax revenues of U.S. municipalities.

Equity investors still underappreciate the risks and benefits of an ESG mindset and the prospect that regulatory and tax and social change is coming. Moreover, the exposure of stocks versus bonds to the benefits and risk mitigation of ESG practices is different. The fundamental value of a bond depends only on the ability to repay fixed principal and interest, while an equity claim reaps the full upside of improving fundamentals and the full downside of the realization of unanticipated risks.

While in the municipal bond markets we see a small premium price on green securities, in the equity markets where fundamental value is much harder to estimate away from the streetlight, we believe that investors are only beginning to wake up to the potential benefits of positive environmental practices. These practices could generate profit and reduce risk, capturing the benefits of technological innovation, avoiding the costs of environmental disasters, and preparing for future public policy that will sap demand for legacy, carbon emitting technologies. While this is harder to prove in equity markets, we at Acadian believe that the equity markets are still in the early innings when it comes to the efficient pricing of these opportunities and risks.

Endnotes

- One strand of the academic literature takes this point of view. For example, Renneboog, Ter Horst, and Zhang (2008) find that investors are willing to accept lower returns in exchange for social objectives. This is consistent with the findings of Hong and Kacperczyk (2009) that so-called sin stocks earn above average returns. Recent papers by Oehmke and Opp (2019), Pastor, Stambaugh, and Taylor (2019) and Pedersen, Fitzgibbons, and Pomorski (2019) also take this view.

- Another strand of the academic literature takes the second and third points of view. For example, in a survey of investors, Amel-Zadeh and Serafaim (2018) report that relevance to investment performance is the most frequent driver of the use of ESG data.

- The category of “green bond” is not as well-defined as “S&P 500 stocks” but not as fuzzy as “junk bonds” or “growth stocks.” We (Baker et al. 2020) use the CUSIP-level Bloomberg green bond tag as the first step for our sample of U.S. corporate and municipal bonds as an objective, replicable identification method that meets institutional standards. We also add municipal green bonds identified by Mergent.

- Larcker and Watts (2019) go so far as to say that this means that there is no green bond premium, because green and ordinary bonds issued by the same issuer on the same day have comparable yields. Our analysis suggests that there is a premium but one that spills over on the date of issuance, where issuers are reluctant to extract a premium price on their green bonds.

- The jury is out in the academic literature. For example, Hong and Kacperzyk (2009) suggest that “sin stocks” trade at a discount and display higher average returns, whereas Blitz and Fabozzi (2017) attribute these findings to other characteristics.

Legal Disclaimer

These materials provided herein may contain material, non-public information within the meaning of the United States Federal Securities Laws with respect to Acadian Asset Management LLC, Acadian Asset Management Inc. and/or their respective subsidiaries and affiliated entities. The recipient of these materials agrees that it will not use any confidential information that may be contained herein to execute or recommend transactions in securities. The recipient further acknowledges that it is aware that United States Federal and State securities laws prohibit any person or entity who has material, non-public information about a publicly-traded company from purchasing or selling securities of such company, or from communicating such information to any other person or entity under circumstances in which it is reasonably foreseeable that such person or entity is likely to sell or purchase such securities.

Acadian provides this material as a general overview of the firm, our processes and our investment capabilities. It has been provided for informational purposes only. It does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or to purchase, shares, units or other interests in investments that may be referred to herein and must not be construed as investment or financial product advice. Acadian has not considered any reader's financial situation, objective or needs in providing the relevant information.

The value of investments may fall as well as rise and you may not get back your original investment. Past performance is not necessarily a guide to future performance or returns. Acadian has taken all reasonable care to ensure that the information contained in this material is accurate at the time of its distribution, no representation or warranty, express or implied, is made as to the accuracy, reliability or completeness of such information.

This material contains privileged and confidential information and is intended only for the recipient/s. Any distribution, reproduction or other use of this presentation by recipients is strictly prohibited. If you are not the intended recipient and this presentation has been sent or passed on to you in error, please contact us immediately. Confidentiality and privilege are not lost by this presentation having been sent or passed on to you in error.

Acadian’s quantitative investment process is supported by extensive proprietary computer code. Acadian’s researchers, software developers, and IT teams follow a structured design, development, testing, change control, and review processes during the development of its systems and the implementation within our investment process. These controls and their effectiveness are subject to regular internal reviews, at least annual independent review by our SOC1 auditor. However, despite these extensive controls it is possible that errors may occur in coding and within the investment process, as is the case with any complex software or data-driven model, and no guarantee or warranty can be provided that any quantitative investment model is completely free of errors. Any such errors could have a negative impact on investment results. We have in place control systems and processes which are intended to identify in a timely manner any such errors which would have a material impact on the investment process.

Acadian Asset Management LLC has wholly owned affiliates located in London, Singapore, and Sydney. Pursuant to the terms of service level agreements with each affiliate, employees of Acadian Asset Management LLC may provide certain services on behalf of each affiliate and employees of each affiliate may provide certain administrative services, including marketing and client service, on behalf of Acadian Asset Management LLC.

Acadian Asset Management LLC is registered as an investment adviser with the U.S. Securities and Exchange Commission. Registration of an investment adviser does not imply any level of skill or training.

Acadian Asset Management (Singapore) Pte Ltd, (Registration Number: 199902125D) is licensed by the Monetary Authority of Singapore. It is also registered as an investment adviser with the U.S. Securities and Exchange Commission.

Acadian Asset Management (Australia) Limited (ABN 41 114 200 127) is the holder of Australian financial services license number 291872 ("AFSL"). It is also registered as an investment adviser with the U.S. Securities and Exchange Commission. Under the terms of its AFSL, Acadian Asset Management (Australia) Limited is limited to providing the financial services under its license to wholesale clients only. This marketing material is not to be provided to retail clients.

Acadian Asset Management (UK) Limited is authorized and regulated by the Financial Conduct Authority ('the FCA') and is a limited liability company incorporated in England and Wales with company number 05644066. Acadian Asset Management (UK) Limited will only make this material available to Professional Clients and Eligible Counterparties as defined by the FCA under the Markets in Financial Instruments Directive, or to Qualified Investors in Switzerland as defined in the Collective Investment Schemes Act, as applicable.