Many multi-factor quantitative equity strategies that incorporate value, quality, and momentum signals have struggled over the past year. While certain formulations of value have suffered even more protracted underperformance, momentum and quality had, until recently, helped to offset the impact. That’s not surprising—we expect these factors to diversify one another, especially value and momentum, which over the long term have been negatively correlated. Against that historical backdrop, the simultaneous under-performance of these factor groups in recent months is unprecedented.

In this note, we document just how anomalous the breakdown in factor diversification has been. We offer perspective on its causes and the implications for investors.

Context for Recent Factor Performance

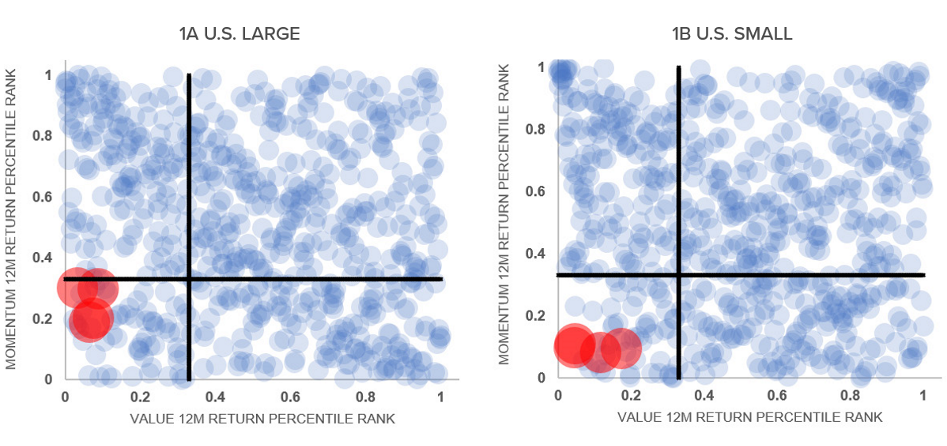

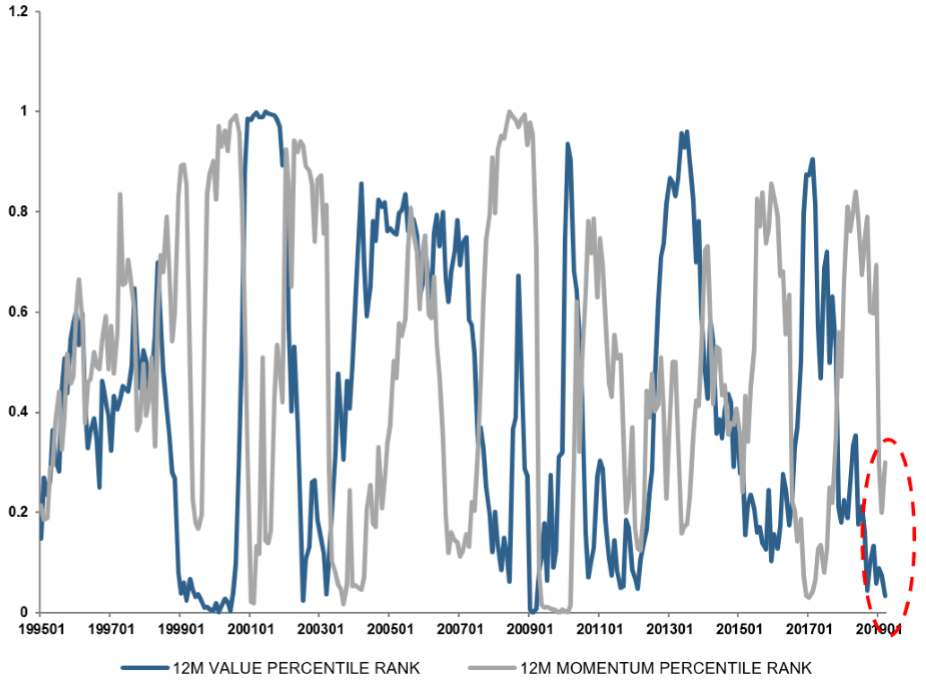

Figure 1 provides a compact picture of the recent poor performance of both value and momentum in U.S. equities. Specifically, it shows rolling twelve-month factor portfolio returns expressed as percentile ranks relative to their long-term historical distributions.

Percentile ranks of factor returns based on twelve-month overlapping windows from July 1963-April 2019. Red dots indicate 12m returns for Jan 2019-Apr 2019. Solid dark lines indicate 33rd percentiles. See Appendix A for details on factor construction and returns calculation. Sources: Calculated from monthly factor returns as found in the “6 Portfolios Formed on Size and Book-to-Market (2 x 3)” and “6 Portfolios Formed on Size and Momentum (2 x 3)” files at Kenneth R. French’s data library. Copyright 2019 Kenneth R. French. All Rights Reserved. This is meant to be an educational example and does not represent investment returns generated by an actual portfolio. Results do not reflect actual trading or an actual account. Results do not reflect transaction costs or other implementation costs and do not reflect advisory fees or their potential impact. Hypothetical results are not indicative of actual future results. Every investment program has the opportunity for loss as well as profit.

Although we’ve based the exhibit on simple Fama-French factor specifications, because they’re well known and offer extensive returns histories, we believe that the aspects of their recent behavior highlighted in this discussion apply to a wide range of more refined specifications employed in practice by active multi-factor investors.1

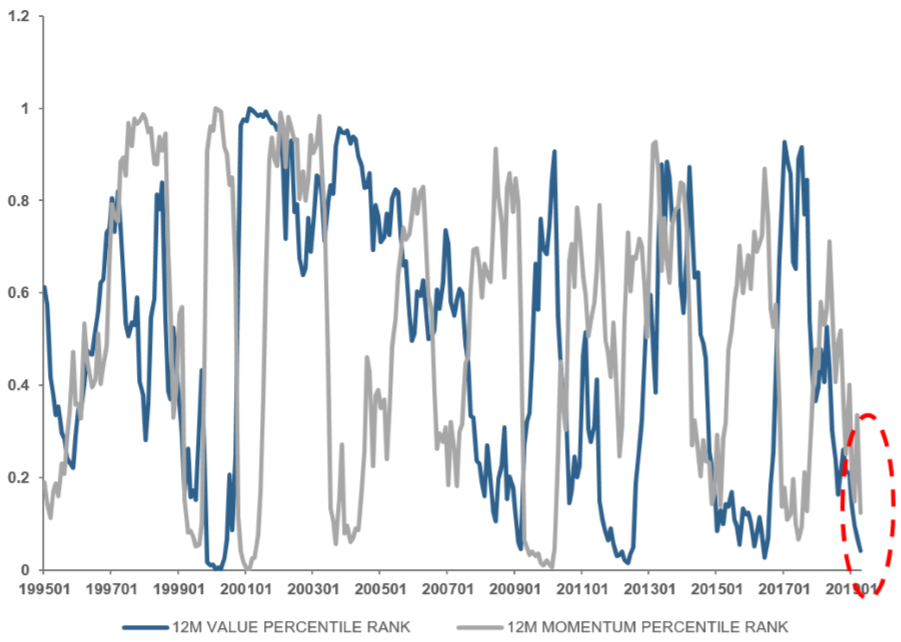

Highlighting the most recent data points in red, Figure 1A shows that for U.S. large-cap stocks, the performance of value over the past twelve months represents a 7th percentile outcome (position on the x-axis).2 That is, since 1963, we’ve only seen worse returns from value about 7% of the time. Similarly, momentum’s recent performance also hasn’t been good, a 19th percentile historical outcome (position on the y-axis). In U.S. small-cap stocks, Figure 1B, the most recent value and momentum returns look even more anomalous, ranking as 5th and 10th percentile outcomes, respectively.

The clouds of blue dots in the scatter charts clearly demonstrate the diversification that value and momentum have provided historically: when one factor has performed poorly, the other often has performed well. Appendix B Figures B1 and B2 clearly document the negative relationship between their returns.

But the two factors haven’t diversified each other over the past year. In fact, while the recent performances of value and momentum have been unusually poor individually, their simultaneous performance has been especially anomalous. For small-cap stocks, in fact, it is unprecedented over the past fifty years. We’ve never seen worse joint performance of value and momentum than during the past 12 months ending April 2019, as evidenced by the red dot in the bottom-left corner of Figure 1B.

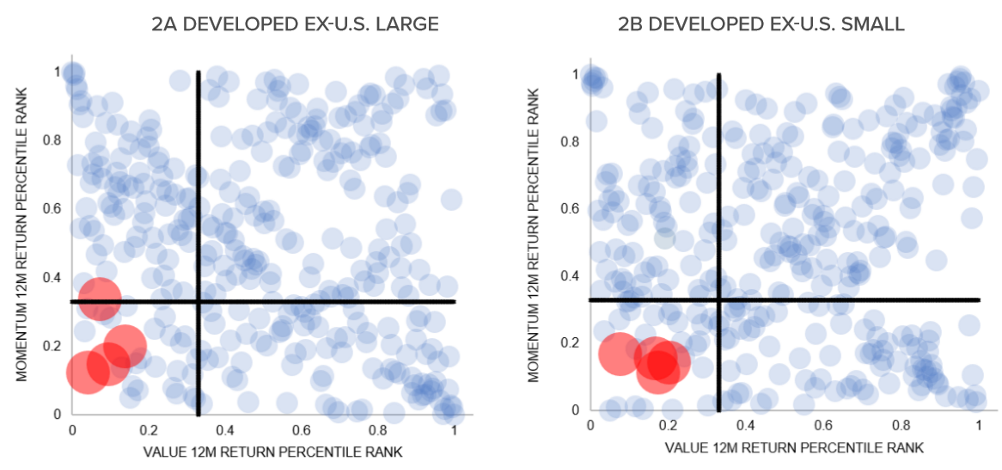

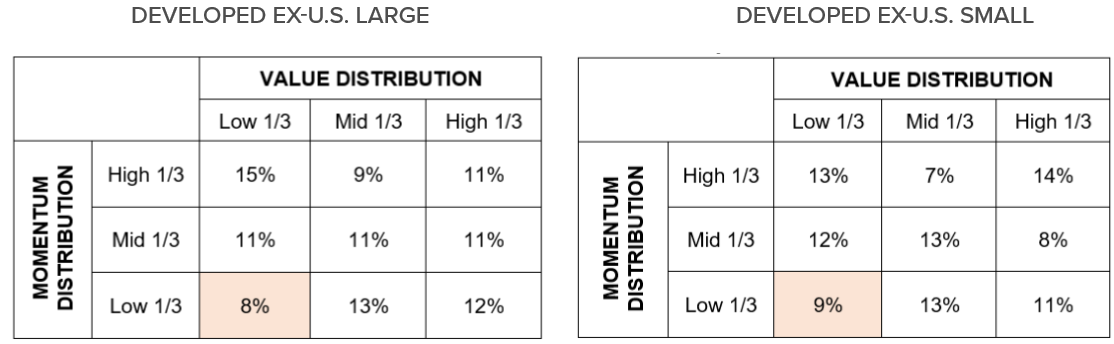

The general picture applies globally, not just to the U.S. Appendix B Figures B3-B5 provide analogous results for Developed ex-U.S. large- and small-cap stocks.

Extending the analysis to quality, recent factor performance among U.S. small-cap stocks looks even more unusual. Within that universe, returns to a generic quality formulation over the past twelve months represent only a 10th percentile historical outcome.3 To contextualize quality performance in combination with the historically poor returns of value and momentum, since 1963 we’ve only seen returns of the three factors simultaneously fall into the bottom third of their individual distributions roughly 4% of the time, let alone see concurrent 7th, 19th, and 10th percentile outcomes.

An Interpretation

In the U.S., we view the recent breakdown in factor diversification as the interaction between 1) a reinvigorated preference for growth stocks driven by the Fed’s Q1 pivot back towards easing, a continuation of a trend that has been in place since the global financial crisis, and 2) inherently path-dependent behavior of traditional price momentum signals that were whipsawed by the market’s Q4 2018 tumble and 2019 recovery.

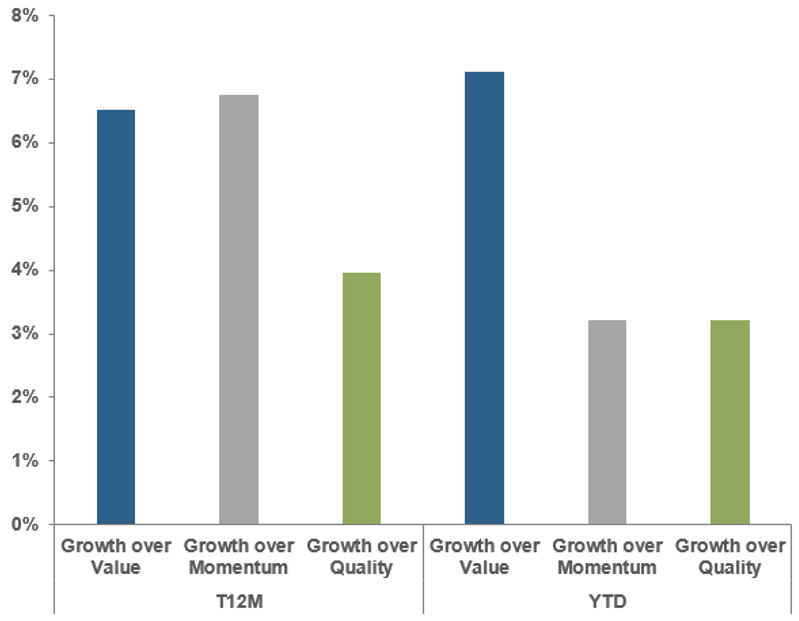

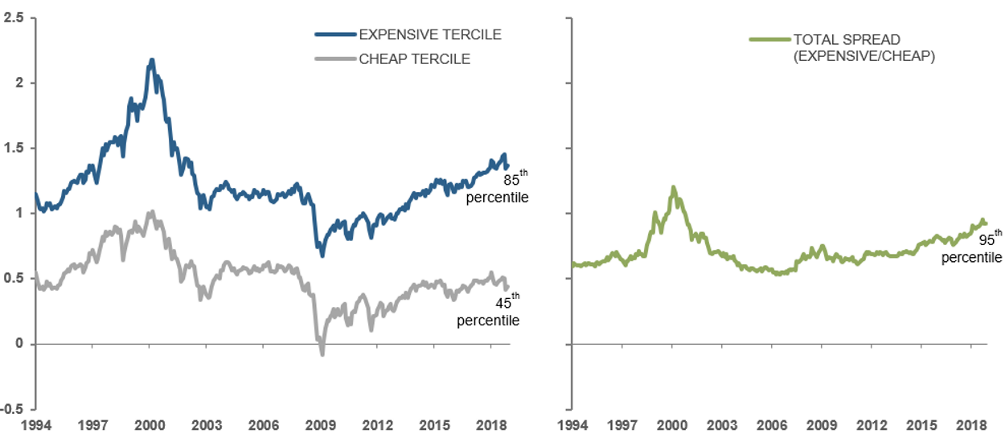

Reflective of the first observation, at the same time that value, momentum, and quality have struggled, investors have favored growth. Figure 2 shows that MSCI’s U.S. Growth Index, whose construction incorporates measures of both trailing and forward fundamental growth, has materially outperformed the corresponding definitions of Value, Momentum, and Quality indexes in recent months. Further, Figure 3 shows that over the first few months of the year, P/B valuations of the most expensive U.S. stocks have snapped back close to late 2018 highs. Arguably, the Fed’s shift headed off conditions that could have led to a more severe reversion of valuations, and it renewed pressures on investors to target growth opportunities even at expensive valuations by historical standards.

USD net total returns to MSCI USA Growth, MSCI USA Value, MSCI USA Momentum, WisdomTree Earnings Weighted Index (to be consistent with Fama-French use of gross margins-based Quality). Sources: Acadian, Bloomberg, MSCI. Copyright MSCI 2019. All Rights Reserved. Unpublished. PROPRIETARY TO MSCI. For illustrative purposes only. It is not possible to invest directly in an index. Every investment program has the opportunity for losses as well as profits. Past results are not indicative of future results.

Chart shows P/B of top and bottom tercile stocks in Acadian’s North American equity universe. Spread is defined as the ratio between the two measures. Shown on a log scale. Sources: Acadian analysis, Bloomberg, MSCI. Copyright MSCI 2019. All Rights Reserved. Unpublished. PROPRIETARY TO MSCI. For illustrative purposes only. Every investment program has the opportunity for losses as well as profits

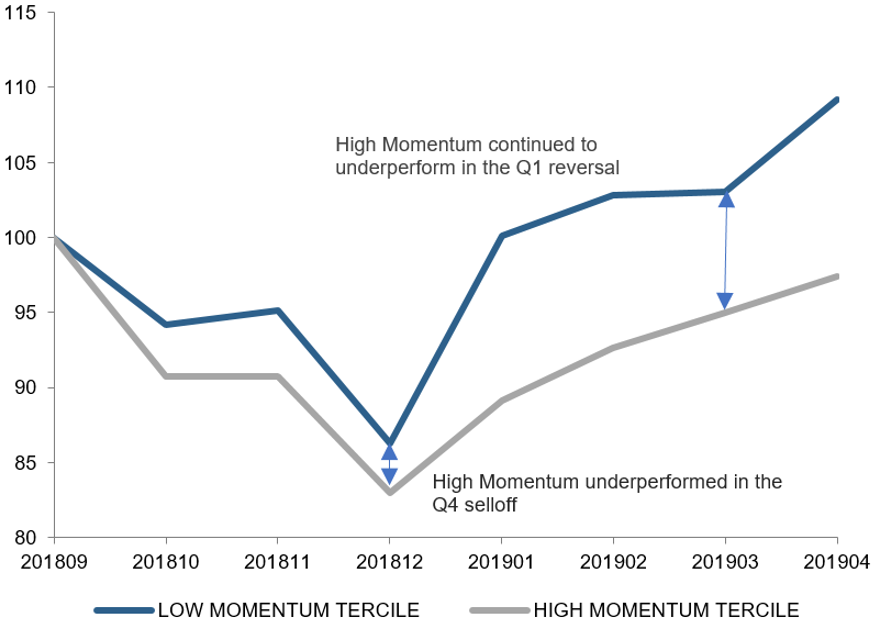

In support of the second observation, regarding the behavior of price momentum, Figure 4 examines the performance of momentum during the Q4 2018 market sell-off and subsequent recovery. Two features stand out. First, during the Q4-Q1 market whipsaw, momentum seems to have been initially stung by an overweight to early 2018 outperformers that suffered during the Q4 selloff and then hurt again by reduced weighting to these stocks during their recovery in Q1 2019. Second, the Q4 momentum drawdown, while severe, hardly qualifies as a momentum “crash,” which we might typically associate with a more pronounced turn in the business cycle and a more significant reversion of valuations that would have been associated with a material payoff to a P/B-based value factor.

Data are for stock returns, observed at monthly frequency, over the “modern sample,” which is July 1963-April 2019 for the U.S. We use returns for common stocks traded on NYSE, AMEX, and, after 1973, NASDAQ. For illustrative purposes only. Performance rebased to 100 as of September 30th, 2018. Sources: Acadian analysis, the Center for Research in Securities Prices (CRSP) at the University of Chicago, as curated and published by Kenneth R. French. Copyright 2019 Kenneth R. French. All Rights Reserved. For illustrative purposes only. Every investment program has the opportunity for losses as well as profits. Past results are not indicative of future results.

Implications

Based on the above interpretation, we see risk in overreacting to the recent poor simultaneous performance of value, momentum, and quality. Its historical aberrance doesn’t indicate that multi-factor quant approaches are broken or that such factors will be highly correlated going forward, as we might expect if quant were overcrowded.

In fact, we currently see wide valuation spreads in the U.S. market, close to those last seen during the Technology, Media, Telecom (TMT) bubble, as a healthy indicator for quant strategies. Although certain economic scenarios could unfold that might justify these wide value spreads ex-post, we do not believe that investors are better now at extrapolating fundamentals than they have been in the past. In other words, we believe that the behavioral biases associated with the existence of a long-term valuation premium continue to persist, and we interpret the valuation spread as a measure of the associated opportunity set.

But investors’ behavioral biases are expressed in a complex economic and policy environment, which, among other things, makes factors difficult to time and may cause material and protracted drawdowns in their performance. For certain formulations of value, for example, such drawdowns may be both uncomfortable and inextricably linked with the long-term payoff to the factor. (E.g., value’s performance around the TMT bubble.)

Conclusion

Framed with the above interpretation, the key question raised by recent factor performance isn’t the long-term sustainability of active multi-factor quant approaches. Rather, it’s the vulnerability of taking an unbalanced one-factor bet on growth. We see no reason to abandon a dispassionate, systematic investing approach that capitalizes on mispricing created by other investors’ persistent behavioral biases.

Appendix A: Factor Specifications

The Kenneth R. French dataset defines “value” as the ratio of book value to market value of common shares at the end of June of each calendar year. It defines “momentum” as the trailing returns over the prior twelve months, excluding the most recent month; this characteristic is updated monthly. It defines “quality” at the end of each June as gross margins (revenue less costs of goods sold; sales, general, and administrative expenses; and interest) relative to book value of common shares. In the case of value and quality, the dataset uses relevant accounting data from the latest available annual report with fiscal year end in the prior calendar year.

Factor returns sourced from the Center for Research in Securities Prices (CRSP) at the University of Chicago, as curated and published by Kenneth R. French. Returns are monthly frequency are from July 1963-April 2019 for the U.S. and July 1990-April 2019 for Developed ex-U.S. For the U.S., we use returns for common stocks traded on NYSE, AMEX, and, after 1973, NASDAQ.

Appendix B: Additional Results

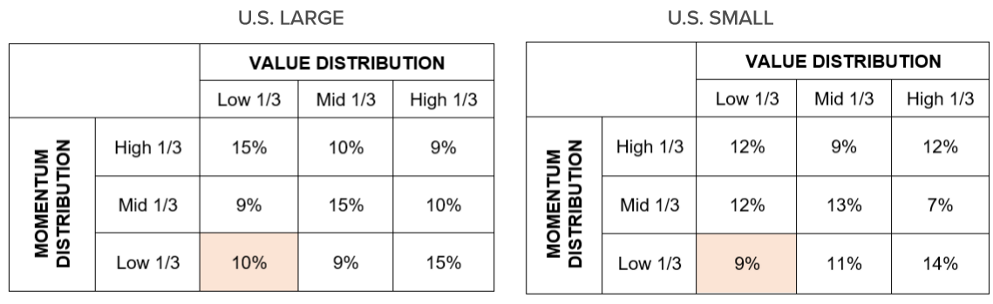

Joint frequencies of factor returns based on twelve-month overlapping windows from July 1963-April 2019. See Appendix A for details on factor construction and returns calculation. Sources: Calculated from monthly factor returns as found in the “6 Portfolios Formed on Size and Book-to-Market (2 x 3)” and “6 Portfolios Formed on Size and Momentum (2 x 3)” files at Kenneth R. French’s data library. Copyright 2019 Kenneth R. French. All Rights Reserved. This is meant to be an educational example and does not represent investment returns generated by an actual portfolio. Results do not reflect actual trading or an actual account. Results do not reflect transaction costs or other implementation costs and do not reflect advisory fees or their potential impact. Hypothetical results are not indicative of actual future results. Every investment program has the opportunity for loss as well as profit.

Joint frequencies of factor returns based on twelve-month overlapping windows from July 1963-April 2019. See Appendix A for details on factor construction and returns calculation. Sources: Calculated from monthly factor returns as found in the “6 Portfolios Formed on Size and Book-to-Market (2 x 3)” and “6 Portfolios Formed on Size and Momentum (2 x 3)” files at Kenneth R. French’s data library. Copyright 2019 Kenneth R. French. All Rights Reserved. This is meant to be an educational example and does not represent investment returns generated by an actual portfolio. Results do not reflect actual trading or an actual account. Results do not reflect transaction costs or other implementation costs and do not reflect advisory fees or their potential impact. Hypothetical results are not indicative of actual future results. Every investment program has the opportunity for loss as well as profit.

Percentile ranks of factor returns based on twelve-month overlapping windows using U.S. Large stocks. Sources: Acadian analysis, the Center for Research in Securities Prices (CRSP) at the University of Chicago, as curated and published by Kenneth R. French. Copyright 2019 Kenneth R. French. All Rights Reserved. For illustrative purposes only. Every investment program has the opportunity for losses as well as profits. Past results are not indicative of future results.

Percentile ranks of factor returns based on twelve-month overlapping windows from July 1990-April 2019. Red dots indicate 12m returns for Jan 2019-Apr 2019. Solid dark lines indicate 33rd percentiles. See Appendix A for details on factor construction and returns calculation. Sources: Calculated from monthly factor returns as found in the “6 Global ex US Portfolios Formed on Size and Book-to-Market (2 x 3)” and “6 Global ex US Portfolios Formed on Size and Momentum (2 x 3)” files at Kenneth R. French’s data library. Copyright 2019 Kenneth R. French. All Rights Reserved. This is meant to be an educational example and does not represent investment returns generated by an actual portfolio. Results do not reflect actual trading or an actual account. Results do not reflect transaction costs or other implementation costs and do not reflect advisory fees or their potential impact. Hypothetical results are not indicative of actual future results. Every investment program has the opportunity for loss as well as profit.

Percentile ranks of factor returns based on twelve-month overlapping windows from July 1990-April 2019. Red dots indicate 12m returns for Jan 2019-Apr 2019. Solid dark lines indicate 33rd percentiles. See Appendix A for details on factor construction and returns calculation. Sources: Calculated from monthly factor returns as found in the “6 Global ex US Portfolios Formed on Size and Book-to-Market (2 x 3)” and “6 Global ex US Portfolios Formed on Size and Momentum (2 x 3)” files at Kenneth R. French’s data library. Copyright 2019 Kenneth R. French. All Rights Reserved. This is meant to be an educational example and does not represent investment returns generated by an actual portfolio. Results do not reflect actual trading or an actual account. Results do not reflect transaction costs or other implementation costs and do not reflect advisory fees or their potential impact. Hypothetical results are not indicative of actual future results. Every investment program has the opportunity for loss as well as profit.

Joint frequencies of factor returns based on twelve-month overlapping windows from July 1990-April 2019. See Appendix A for details on factor construction and returns calculation. Sources: Calculated from monthly factor returns as found in the “6 Global ex US Portfolios Formed on Size and Book-to-Market (2 x 3)” and “6 Global ex US Portfolios Formed on Size and Momentum (2 x 3)” files at Kenneth R. French’s data library. Copyright 2019 Kenneth R. French. For further details on factor definitions, please see Appendix A. This is meant to be an educational example and is not intended to represent investment returns generated by an actual portfolio. Results do not reflect actual trading or an actual account. Results do not reflect transaction costs or other implementation costs and do not reflect advisory fees or their potential impact. Hypothetical results are not indicative of actual future results. Every investment program has the opportunity for loss as well as profit.

Percentile ranks of factor returns based on twelve-month overlapping windows using Developed Ex-U.S. Large stocks. Sources: Acadian analysis, the Center for Research in Securities Prices (CRSP) at the University of Chicago, as curated and published by Kenneth R. French. Copyright 2019 Kenneth R. French. All Rights Reserved. For illustrative purposes only. Every investment program has the opportunity for losses as well as profits. Past results are not indicative of future results.