January 2018

A Problem and an Imperfect Solution

While global markets just posted yet another strong year in 2017, this has likely only furthered concerns about future long-term return prospects. Some recent predictions quote long-term annualized returns as low as 4-5% for equities, and 0-1% for fixed income,1 which would fall well below levels we have become accustomed to over the last few decades, and far below the requirements of many institutions and individuals to meet future spending needs.

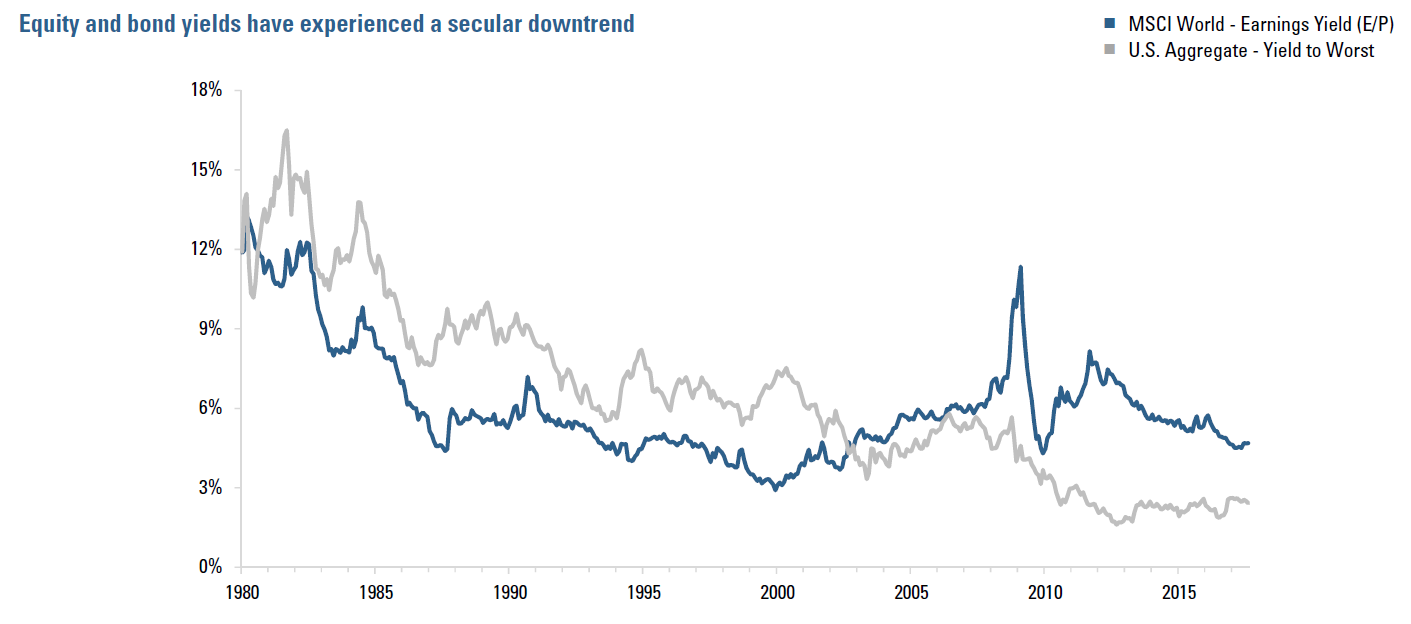

Figure 1 below helps illustrate the problem. A confluence of falling bond yields (from double digit levels in the early 80s) and multiple expansion for equities has driven the strong equity and bond returns of recent decades. However, these tailwinds will likely turn into formidable headwinds, as bond markets face record low yields and the potential adverse price impact from future yield rises. Meanwhile lofty equity valuations (which means low earning yields) leave future earnings growth as the main driver of future equity returns.

Sources: MSCI, Bloomberg. Indices: MSCI World, Bloomberg Barclays US Aggregate Bond

For illustrative purposes only. It is not possible to invest directly in any index. Every investment program has the opportunity for losses as well as profits. Index Source: MSCI Copyright MSCI 2018. All Rights Reserved. Unpublished. PROPRIETARY TO MSCI. Bloomberg Barclays Indices are owned by Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

In an attempt to make up for lost ground, investors may decide to shift portfolio allocations towards riskier, possibly higher returning assets. However, such an approach comes at the price of greater overall risk, while increased equity exposure may leave portfolios more vulnerable to subsequent equity sell-offs.

MACS in a Nutshell

Faced with potential headwinds for traditional equity/ bond portfolios, asset owners have been on the hunt for alternative, uncorrelated sources of return, which could potentially generate much-needed returns, while diversifying away from equity risk. Multi-Asset Class Strategies (“MACS”) offer a possible solution, attracting investors with the potential for shallower drawdowns that do not necessarily coincide with equity bear markets. These types of strategies typically invest in various liquid asset classes and seek to generate excess returns from both active allocation across asset classes and active positioning within them.

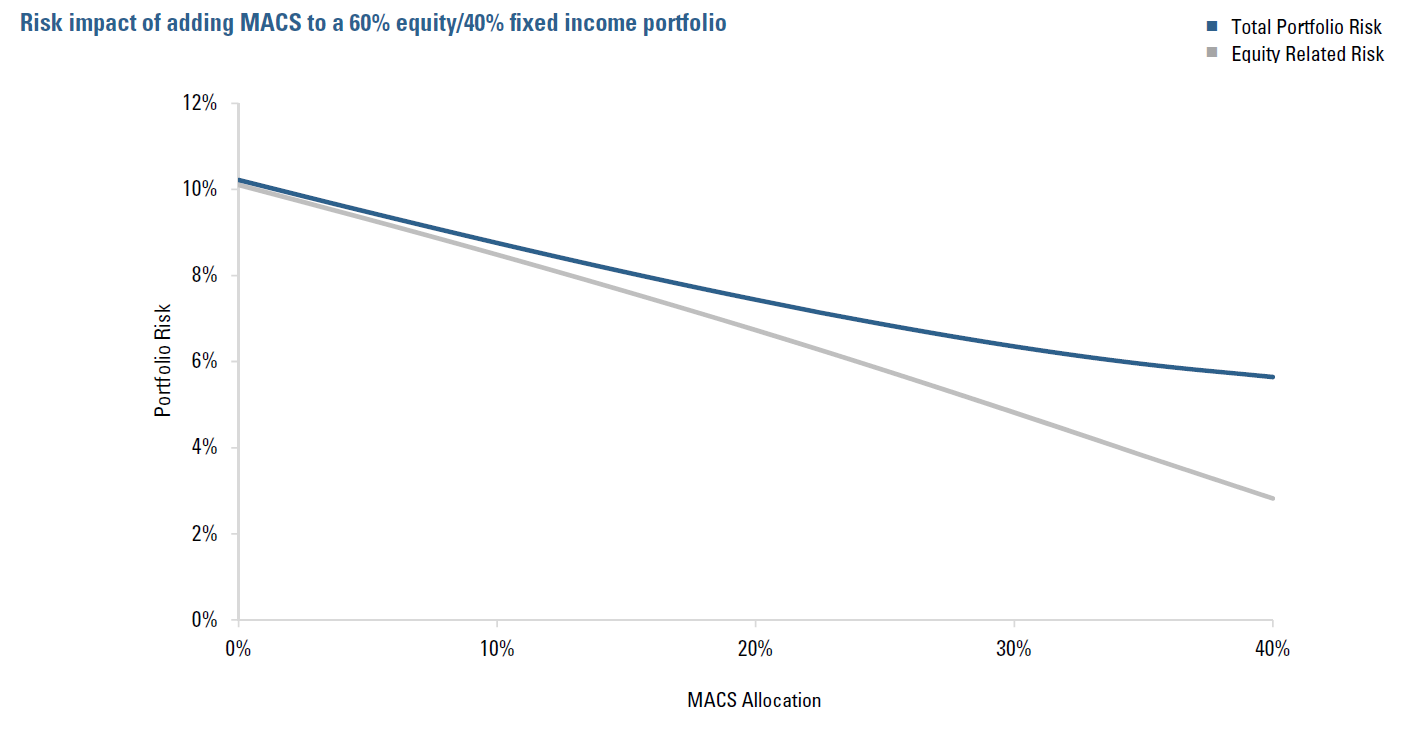

To illustrate the role of MACS in building more robust portfolios, Figure 2 below shows resulting hypothetical portfolio risk as a MACS allocation gets gradually increased, from an assumed starting point of a 60/40 portfolio (upper left-hand corner). MACS has low correlations with the hypothetical portfolio overall and with equities in particular, so funding MACS out of equities will decrease both the overall risk of the resulting portfolio and the risk contributed from equity related sources. As the MACS allocation grows, its diversification benefit to the portfolio starts to diminish, as indicated by the flattening blue line, while the equity contribution continues to drop.

Coping With Complexity

MACS investing involves the complexity of having to navigate across and within a number of heterogeneous asset classes. Some basic approaches address this challenge by repackaging existing standalone single-asset-class capabilities (in equity, fixed income, currency, etc.) into a combined framework. These types of approaches start out with separate portfolios for each asset class, then combine them from the top down.

Such siloed approaches mirror the traditional structure of investment firms, where it is not atypical to see fixed income, equity and currency teams located on different floors—if not in different cities or countries. Each area has its own investment philosophy and is generally focused on a different outcome. Simply shoehorning such disparate single asset class expertise together does not represent a truly coherent approach to multi-asset investing. It may miss return-enhancing opportunities, create risk management challenges, and limit flexibility to customize portfolios to meet investor needs.

Source: Acadian

For illustrative purposes only. This is meant to be an educational illustrative example of hypothetical contribution from equity risk to a 60/40 hypothetical portfolio where we gradually switch assets from Equities to MACS. It is not intended to represent investment results generated by an actual portfolio. They do not represent actual trading or an actual account. Results do not reflect transaction costs, other implementation costs and do not reflect advisory fees or their potential impact. Hypothetical results are not indicative of actual future results. Every investment program has the opportunity for loss as well as profit.

The Need For an Integrated Approach

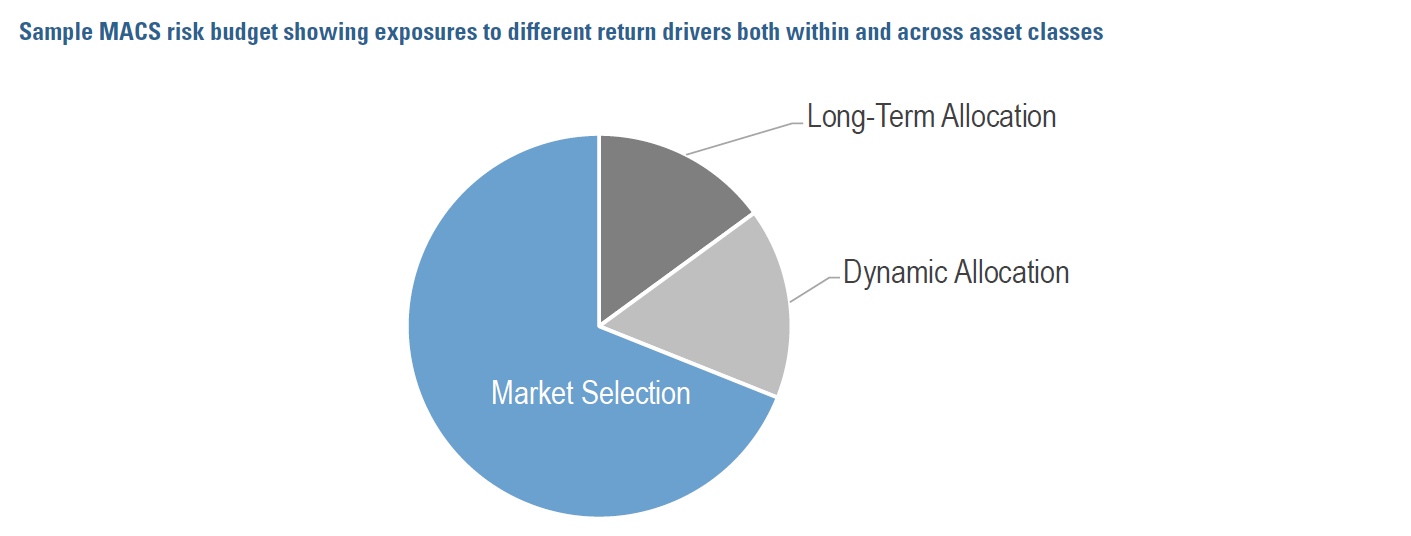

We believe that a more integrated approach, which holistically evaluates markets within asset classes and relationships across asset classes, is better suited to deal with the complexity and the opportunities of multi-asset investing. Such an approach systematically evaluates risk, return and implementation costs for all markets and asset classes simultaneously. Modern quantitative methods greatly help to model the inherent complexity effectively, and allow for comparisons within and across asset classes in an objective and consistent way. In particular, this type of methodology provides greater investment breadth, allowing portfolios to take fuller advantage of potential opportunities, via thousands of signals, forecasts and decisions across a large universe of assets.

Expanding The Opportunity Set

An integrated approach to MACS investing seeks to capture both the idiosyncratic nature of individual asset classes and the relationships across these asset classes. This requires an expanded universe of factors for return forecasting: Asset-specific factors seek to capture return drivers within asset classes, such as value, momentum, carry, and quality, each adapted to reflect the distinct nature of its respective asset class, while macro factors seek to capture cross-asset-class effects.

How exactly to construct such macro factors involves some subtlety. Standard economic data has limitations as a forecasting tool, due to its lagged and backward-looking nature. However, Acadian’s research has shown that market-priced metrics—in particular, measures of cross-asset momentum—can serve as indicators of macro conditions that are predictive of future asset prices. This allows themes like growth, stimulus and inflation to be defined by market prices and incorporated into a multi-asset framework in a timely and actionable way, enhancing the potential for predicting asset returns.

Emphasizing Risk

Taking diverse assets and forecasts and combining them into a robust portfolio requires particular attention to risk. Individual asset classes may behave quite differently, and their underlying assets may interact in surprising ways, possibly leading to portfolios with undesirable risk exposures. Portfolio positions need to be understood in terms of the risk they contribute, and how this aligns with potential returns. The ability to go long/short is a helpful tool to tailor exposures and mitigate unwanted risks, with the goal of maintaining low correlations at the overall portfolio level with respect to traditional and alternative betas. Indeed, positioning defensively in an effort to limit the impact of market drawdowns, is essential to realizing the full benefit of a MACS investment.

The information provided is for illustrative purposes only based on proprietary models. There can be no assurance that the forecasts will be achieved.

Flexible Implementation

We view modern MACS more as a capability than an off-the-shelf product, namely a skills-based approach that can be engineered to achieve specific investor outcomes. This capability is greatly facilitated through the use of listed derivatives in a long/short implementation, which increases flexibility and efficiency to achieve asset class and market exposures. Moreover, nimble implementation may enhance return opportunities and result in more efficient risk control. Well-implemented MACS strategies represent a best-of-both-worlds approach, borrowing investor focus and bespoke implementation from the “institutional, long-only world,” and looking to the model of the “hedge-fund world” for efficient implementation of investment ideas.

A Changing Landscape

Acadian’s new multi-asset capability reflects of a number of developments in the investment industry. One, that outcome-oriented investing is an expanding and enduring trend. Investors can no longer afford to set a basic asset allocation with off-the-shelf investment strategies and hope for the best. They are increasingly looking to the funding needs of their plan first, and working actively with a broad range of investment options to craft a program specifically tailored to a desired result.

Two, MACS underscores the role that systematic investment approaches are increasingly playing in the mainstream. As investors look globally across multiple asset classes and types of implementations, it is too challenging for a traditional investment approach to acquire and analyze sufficient information to gain a forecasting edge and manage risk exposures effectively. However, expertise in each asset class is required to build an effective multi-asset investment process.

Three, institutions are getting better and better at working productively with managers to obtain the strategies and outcomes they need. Increasingly sophisticated institutional staff want ever more opportunity to fine-tune and customize. They want to work with managers who offer platforms of capabilities, rather than simply products. MACS is just one example of a customizable, creative solution to a low return environment. The trend is toward demand for many more.