Quick Take: Crude Below Zero?

Backdrop: a historic imbalance

-

WTI inventories at Cushing, Oklahoma rose during the first three weeks of April at a pace that would exhaust the facility’s working storage capacity in a month.

-

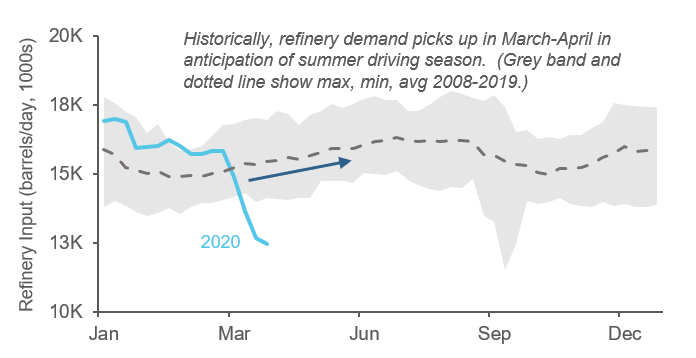

This storage shortage is a measure of what has become a historic supply/demand imbalance. Figure 1 captures the collapse in refiners’ demand as a result of COVID-19, which was accompanied by a burst of OPEC+ exports associated with the Russia-Saudi price war.

A localized market circumstance

-

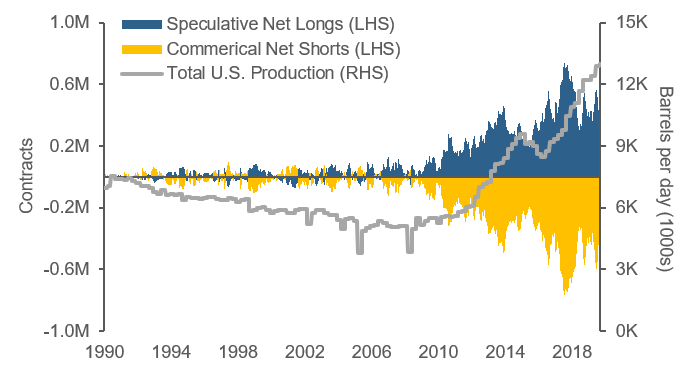

Tuesday’s collapse of WTI May futures to -$37 per barrel reflects two conditions specific to that market: 1) It has experienced substantial growth in open interest as U.S. shale companies have hedged future production with speculative longs taking the other side. (Figure 2) 2) WTI futures settle physically rather than in cash.

-

The historic price drop the day prior to contract settlement reflects the weakness in demand for physical oil and long speculators’ desperation to avoid delivery, which was exacerbated by the shortage of storage capacity.

-

Major commodity indexes and tracking products had already rebalanced into June and July contracts, so a relatively small set of speculators racing for the exits drove the price action. The event was localized to WTI; it didn’t affect Brent futures, which settle in cash and expire on a different schedule.

Key takeaways

-

The market gyrations don’t impact our baseline view on oil. Our models remain bearish given the historically imbalanced state of the physical market, the macroeconomic outlook, sentiment, and other factors.

-

We suspect that the event could affect roll behavior going forward, with market participants becoming more careful about holding concentrated positions in nearby front-month futures and diversifying oil exposure further out on the curve or to other instruments such as Brent and ETPs.

Figure 1: Seasonality in U.S. DOE crude oil total refinery input

Figure 2: Futures positioning by category vs. U.S. total production

Legal Disclaimer

These materials provided herein may contain material, non-public information within the meaning of the United States Federal Securities Laws with respect to Acadian Asset Management LLC, BrightSphere Investment Group Inc. and/or their respective subsidiaries and affiliated entities. The recipient of these materials agrees that it will not use any confidential information that may be contained herein to execute or recommend transactions in securities. The recipient further acknowledges that it is aware that United States Federal and State securities laws prohibit any person or entity who has material, non-public information about a publicly-traded company from purchasing or selling securities of such company, or from communicating such information to any other person or entity under circumstances in which it is reasonably foreseeable that such person or entity is likely to sell or purchase such securities.

Acadian provides this material as a general overview of the firm, our processes and our investment capabilities. It has been provided for informational purposes only. It does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or to purchase, shares, units or other interests in investments that may be referred to herein and must not be construed as investment or financial product advice. Acadian has not considered any reader's financial situation, objective or needs in providing the relevant information.

The value of investments may fall as well as rise and you may not get back your original investment. Past performance is not necessarily a guide to future performance or returns. Acadian has taken all reasonable care to ensure that the information contained in this material is accurate at the time of its distribution, no representation or warranty, express or implied, is made as to the accuracy, reliability or completeness of such information.

This material contains privileged and confidential information and is intended only for the recipient/s. Any distribution, reproduction or other use of this presentation by recipients is strictly prohibited. If you are not the intended recipient and this presentation has been sent or passed on to you in error, please contact us immediately. Confidentiality and privilege are not lost by this presentation having been sent or passed on to you in error.

Acadian’s quantitative investment process is supported by extensive proprietary computer code. Acadian’s researchers, software developers, and IT teams follow a structured design, development, testing, change control, and review processes during the development of its systems and the implementation within our investment process. These controls and their effectiveness are subject to regular internal reviews, at least annual independent review by our SOC1 auditor. However, despite these extensive controls it is possible that errors may occur in coding and within the investment process, as is the case with any complex software or data-driven model, and no guarantee or warranty can be provided that any quantitative investment model is completely free of errors. Any such errors could have a negative impact on investment results. We have in place control systems and processes which are intended to identify in a timely manner any such errors which would have a material impact on the investment process.

Acadian Asset Management LLC has wholly owned affiliates located in London, Singapore, Sydney, and Tokyo. Pursuant to the terms of service level agreements with each affiliate, employees of Acadian Asset Management LLC may provide certain services on behalf of each affiliate and employees of each affiliate may provide certain administrative services, including marketing and client service, on behalf of Acadian Asset Management LLC.

Acadian Asset Management LLC is registered as an investment adviser with the U.S. Securities and Exchange Commission. Registration of an investment adviser does not imply any level of skill or training.

Acadian Asset Management (Singapore) Pte Ltd, (Registration Number: 199902125D) is licensed by the Monetary Authority of Singapore.

Acadian Asset Management (Australia) Limited (ABN 41 114 200 127) is the holder of Australian financial services license number 291872 ("AFSL"). Under the terms of its AFSL, Acadian Asset Management (Australia) Limited is limited to providing the financial services under its license to wholesale clients only. This marketing material is not to be provided to retail clients.

Acadian Asset Management (UK) Limited is authorized and regulated by the Financial Conduct Authority ('the FCA') and is a limited liability company incorporated in England and Wales with company number 05644066. Acadian Asset Management (UK) Limited will only make this material available to Professional Clients and Eligible Counterparties as defined by the FCA under the Markets in Financial Instruments Directive.